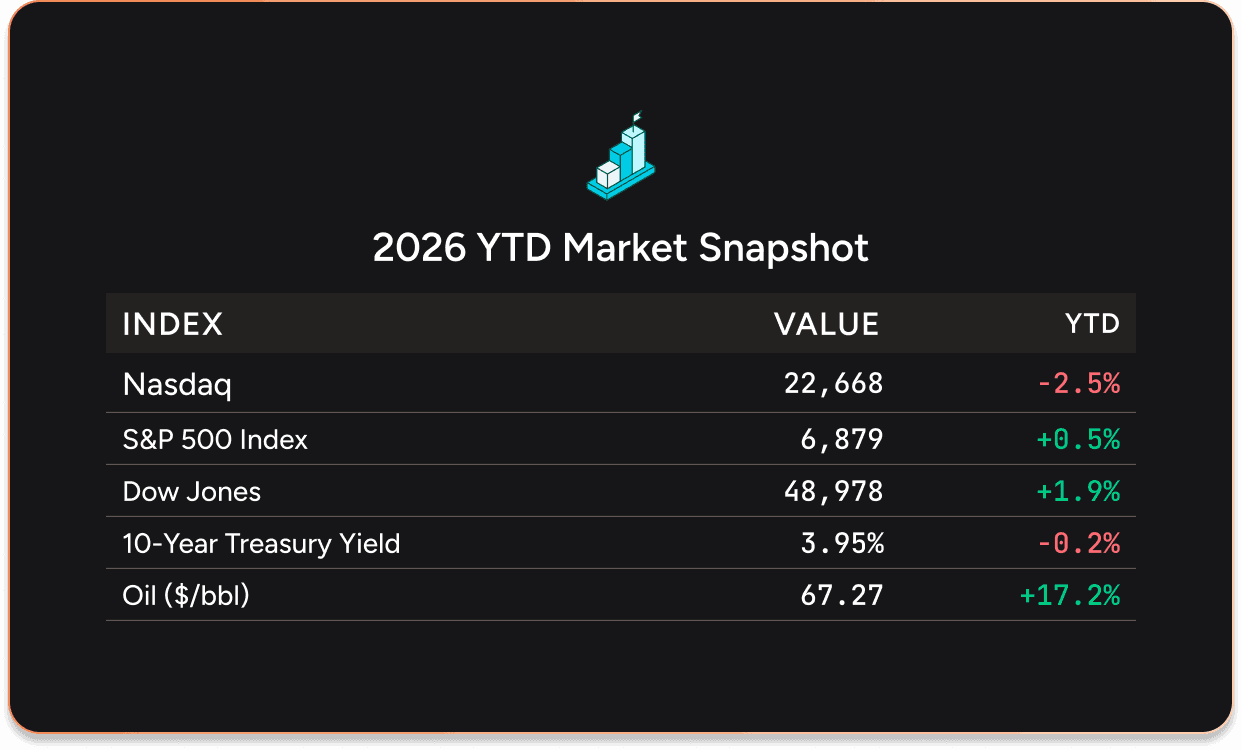

February Ends On A Sour Note, Because Valuations Matter

Mar 2, 2026

•

Lawrence Fuller

Implications From The Bombing Of Iran

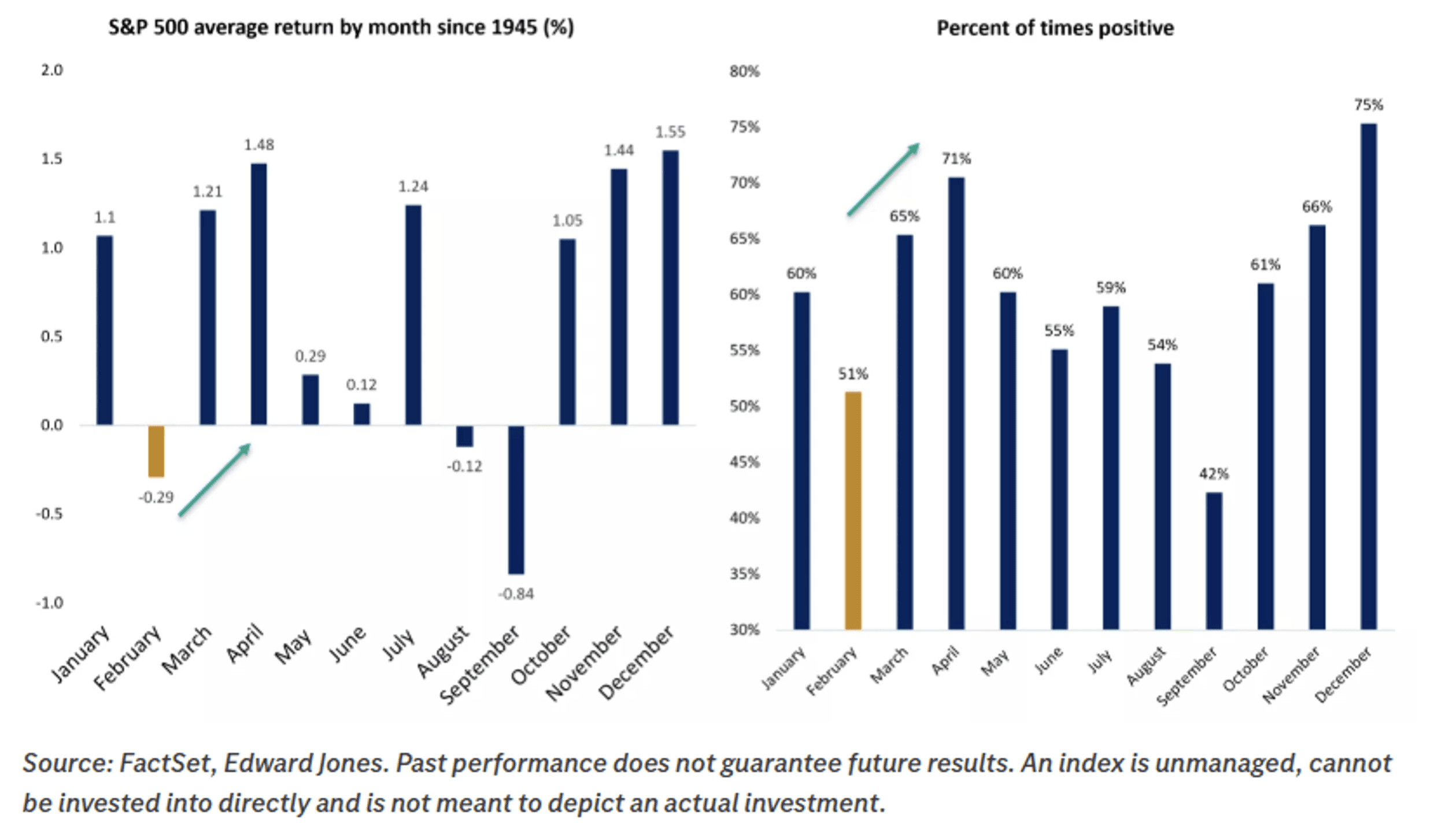

February lived up to its reputation as the second worst performing month of the year for the stock market, as fears that AI could undermine legacy business models continue to linger. There were also renewed concerns about loan losses emerging in private credit lending, which weighed heavily on the financial sector. On the economic front, a hotter-than-expected increase in producer prices for Janaury added insult to injury. The Producer Price Index (PPI) rose 0.5% for the month and 2.9% over the past year. Prices for services rose 0.8%, which was the most since July, reducing expectations for any near term rate cuts by the Federal Reserve. March has historically been a far better month for investors, but it may be treacherous at its start, given the events over the weekend.

The Trump administration ended talks with Iranian officials over its nuclear capabilities and bombed Iran in a coordinated strike with Israel. Leadership was the intial target, and Ayatollah Ali Khamenei is now dead. Oil prices are likely to rise sharply Monday morning, due to concerns about access to the Strait of Hormuz, and may stay eleveated as long as the strikes continue. Historically, from an investment perspective, geopolitical events like this do not end bull markets. They can lead to tremendous short-term volatility, as uncertainty increases dramatically. There will likely be a flight to safety into government bonds, which drives interest rates lower and precious metals higher. Should stock prices fall sharply, I think the worst thing investors can do is sell into an emotional knee-jerk decline. In what will likely be a fluid situation, any meaningful drawdown should be another opportunity to reposition portfolios for higher market levels later this year.

Valuations Are Playing A Pivotal Role In Returns This Year

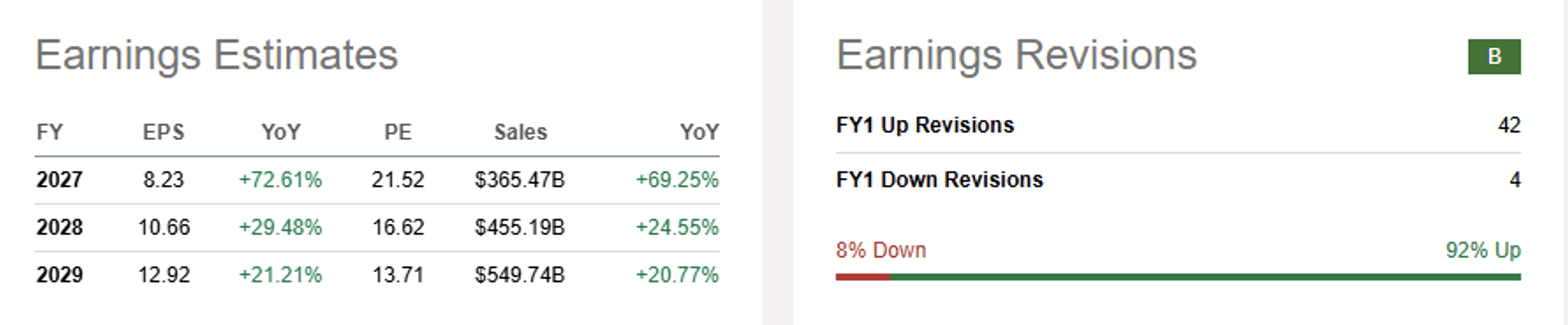

Market bellwether Nvidia, which commands a weighting of 8% in the S&P 500, reported stellar results last week and raised guidance above expectations for the coming year. Why then did its stock price drop 5.5% after earnings and more than 8% on the week? While concerns about future AI capital spending levels persist, I think it has more to do with valuations at a time when investors are shunning many of last year’s momentum plays, scrutinizing future growth prospects, and preparing for a tightening in credit conditions. This spells trouble for companies far less superior than Nvidia, which are trading at multiples of ten times revenues or more with no or limited earnings prospects in the coming year. The rotation from growth to value should continue.

While Nvidia is still one of the preeminent names in the AI space, its earnings and revenue growth are slowing dramatically, which is partly due to its tremendous size. When growth stocks start to realize a deceleration in earnings and revenue growth, no matter how impressive the rates may still be, valuations start to compress. That is what has happened to Nvidia’s stock over the past six months, but the compression has led to much larger losses for many of last year’s high flyers.

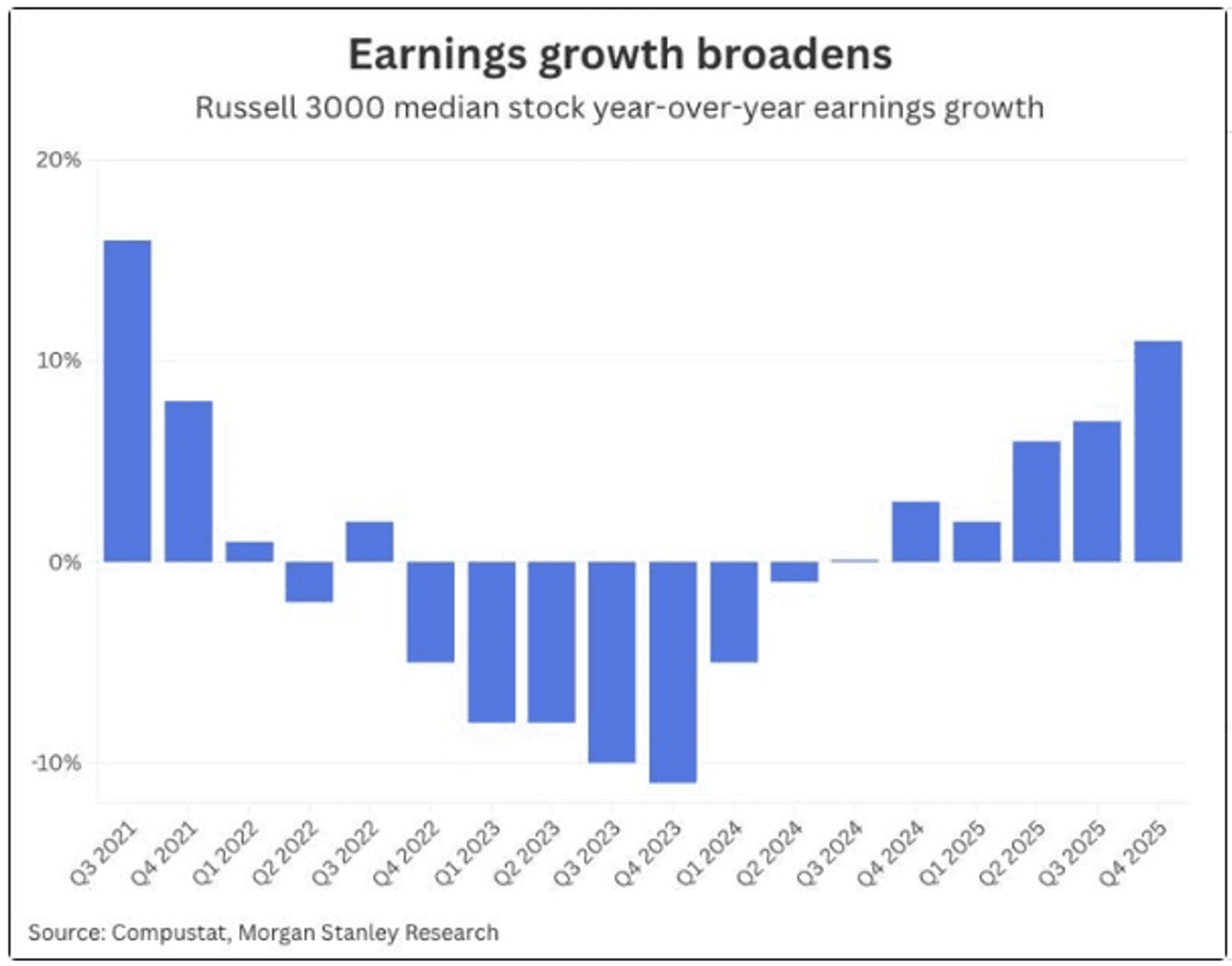

Meanwhile, companies that have lower earnings multiples than the S&P 500’s 22 times, which are realizing accelerating earnings growth, albeit at much lower levels, have been shining. This is evidenced by the outperformance of the average stock within the S&P 500. The equally weighted index has risen 7% this year, while the cap-weighted index that is dominated by the technology sector is flat in 2026. As an economist, market strategist, and stock analyst, I focus intently on rates of change in the data. The direction of change is far more important than the absolute number.

The Russell 3000 index seeks to benchmark the entire stock market. The chart below shows that the earnings growth rate for the median stock in the market nearly doubled in the fourth quarter of last year to a four-year high. This is the most important rate of change underlying the bull market, but it is a function of earnings growth broadening well beyond the technology sector.

Canaries In The Private Credit Coal Mine

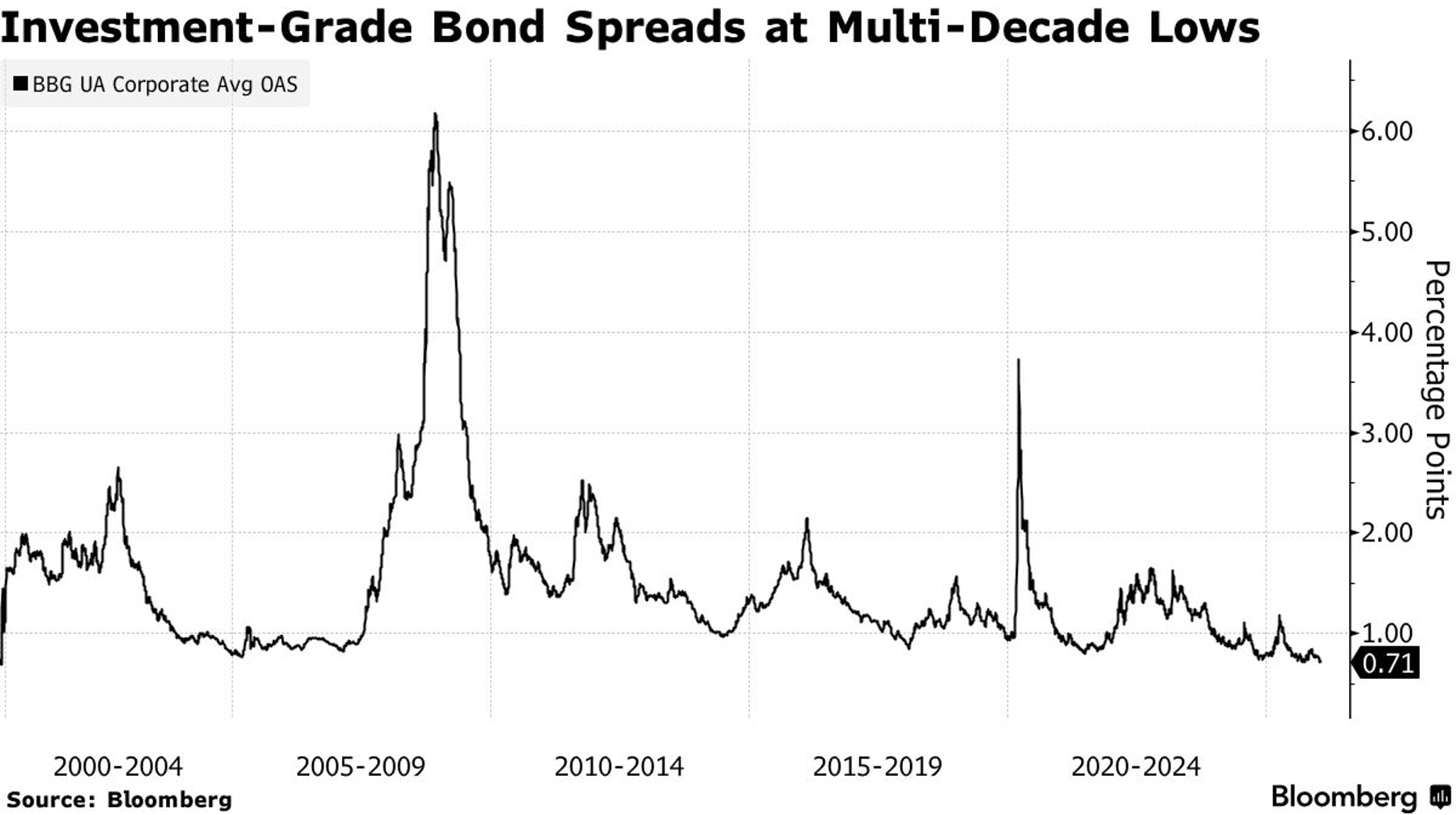

Three weeks ago, I discussed in this newsletter how credit spreads had compressed to near record low levels, which usually coincides with a peak in valuations for the most expensive stocks. Credit spreads measure the difference between what it costs a corporation to borrow money and the cost for the federal government. In other words, it is the difference in yield between a corporate bond and U.S. Treasury bond of the same maturity. This compression led to investment grade bond sales of more than $200 billion in January, which was the fifth largest amount even, as spreads fell to the tightest level since 1998.

Credit spreads started to widen last month, which implies increasing risk for creditors, and higher costs for borrowers. The reason they may widen further is that losses are starting to emerge in the opaque private credit market, which has grown in size to nearly $2 trillion. Private equity firms, business development companies, and other alternative lenders have helped to fuel tremendous growth through lending to private and public companies, presenting meaningful competition for traditional banks that face stiffer regulations. Yet that lack of oversight can lead these lenders to chase returns and ignore risks, as we have seen recently with Blue Owl Capital, Blackstone, and Apollo Global Management. Whether these are one-offs or canaries in the private lending coal mine is difficult to determine, and because their loans are privately held they do not affect the publicly traded credit spreads. Still, spreads are likely to continue widening, which would weigh most heavily on the most expensive growth stocks. Especially those that have no earnings or limited cash flows and rely on borrowing to fund their future growth. This should be an important consideration when selecting stocks to own.

In aggregate, I remain optimistic about the bull market, but leadership is changing as investors rotate from growth to value, seeking lower-risk alternatives to the technology stocks that fueled the gains of the past three years. This bifurcation has created a stock pickers market, which is an ideal playing field for astute investors who do their homework. As I have said before, diversification across sectors, styles, and market caps should be one of the keys to outperforming the broad stock market indices this year.

Lawrence Fuller

Founder of Fuller Asset Management & dub Portfolio Creator SeekingAlpha Top Contributor (22k followers)

Background

With three decades of experience in portfolio management, Lawrence commenced his career at Merrill Lynch in 1993 and subsequently held similar roles at various Wall Street firms before establishing Fuller Asset Management in 2005. Since 2013, he has been an esteemed contributing writer for Seeking Akpha, authoring the widely followed Morning Brief newsletter, which boasts a dedicated readership exceeding 22,000 investors.

© 2026 DASTA Incorporated. All Rights Reserved. Performance shown is gross of fees and does not include SEC and TAF fees paid by customers transacting in securities. The dub app is owned and operated by DASTA Inc.. Advisory services provided by Dub Advisors, an SEC registered investment advisor. Past Performance does not guarantee future results. This content is provided for informational purposes only and is not intended as and may not be relied on in any manner as a recommendation or endorsement of any user, portfolio, thematic idea, or ESG factor offered by DASTA Incorporated (DBA “dub”) or its subsidiaries or affiliates (together “dub”). All investments involve risk, including the possible loss of principal. Past performance does not guarantee future results, and investors should consider their own investment goals, risk tolerance, and financial situation before investing. The content herein is not warranted as to completeness or accuracy and is subject to change. The information presented, and its importance is an opinion only and should not be relied upon as the only important information available. The information may contain forward looking statements, including assumptions, estimates, projections, opinions, models and hypothetical performance analysis, which are inherently subjective. Changes thereto and/or consideration of different or additional factors could have a material impact on the statements made herein and Dub assumes no liability for the information provided. Advisory services provided by DASTA Investment, LLC (“Dub Advisors”), an SEC-registered investment adviser. Brokerage services provide by Dub Financial, LLC, and clearing and execution services by APEX Clearing Corporation (“Apex”), both SEC-registered broker-dealers and members of FINRA/SIPC. The registrations and memberships above in no way imply that the SEC, FINRA, or SIPC has endorsed the entities, products or services discussed herein. Additional Information is available upon request.