It’s All About Oil

Mar 16, 2026

•

Lawrence Fuller

The War In Iran Escalates

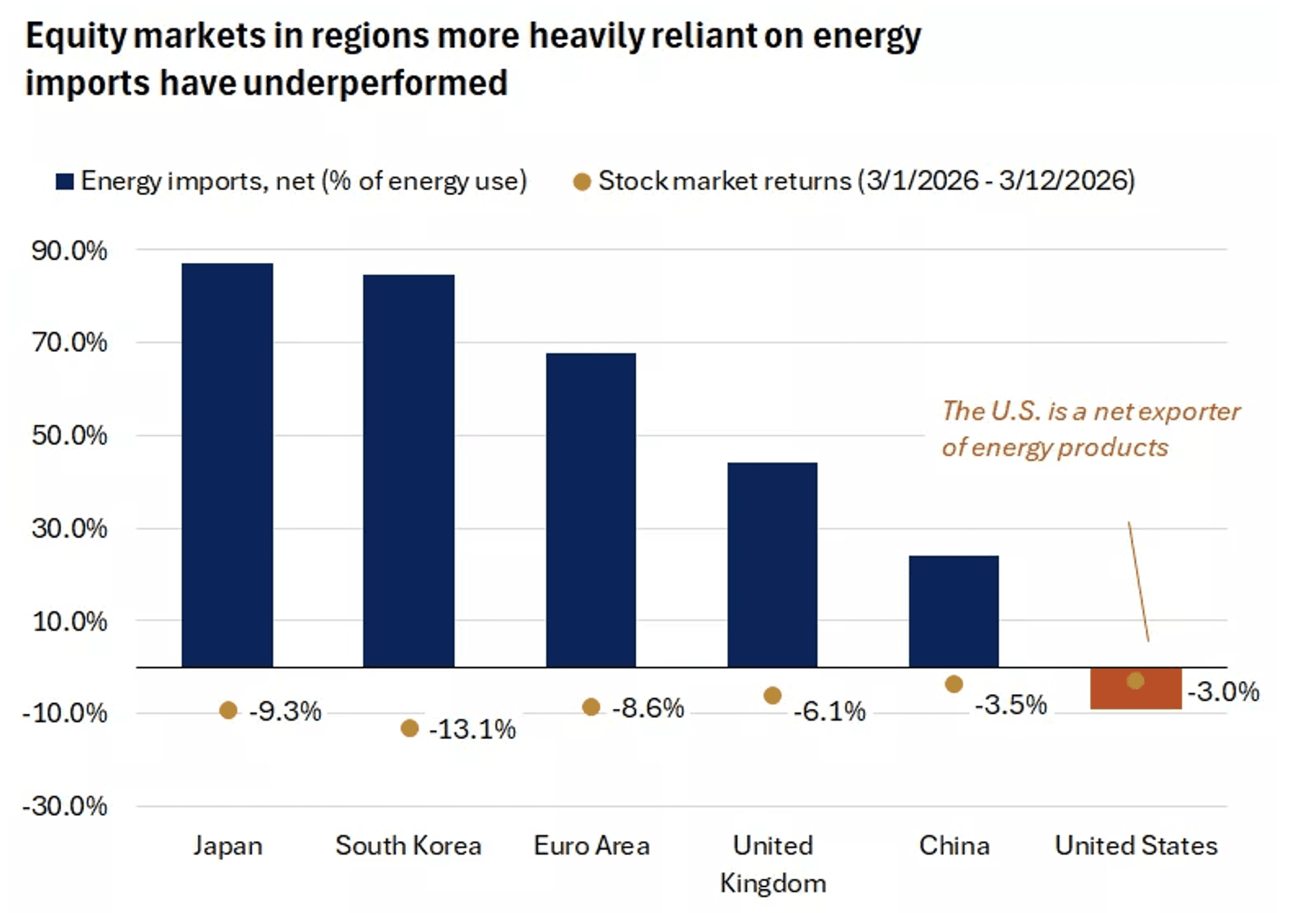

The war in the Middle East moves into its third week with no signs of deescalation. As a result, the price of oil continues to surge with WTI crude hovering near $100 per barrel, as Iran has effectively closed the Strait of Hormuz through which approximately 20% of the world’s oil supply is transported each day. This has led the major market indexes to bleed lower with the S&P 500 now down 5% from its all-time high, while the Magnificent 7 have corrected a full 10%. These drawdowns are relatively modest, largely because the U.S. is a net exporter of oil. Foreign markets, especially those more dependent on imports that pass through this critical waterway, have suffered greater losses.

The more important reason our markets remain resilient is that most investors expect President Trump to reverse course and deescalate the conflict in reponse to the surge in oil prices similar to the way he did after the S&P 500 plunged 19% in reaction to his “reciprocal” tariff policy. All it took was a tweet to ignite a ferocious rally in the market, and no one wants to be left out of a rebound. I don’t think stocks have suffered enough damage to date to provoke an end to the war in Iran, but should oil prices remain elevated above $100 for another week or more, it will likely have an impact on the course of the conflict.

It isn’t how high oil prices rise, but how long they remain elevated. The longer the price of oil remains above $100, the more likely higher energy costs feed into higher prices for all the goods and services consumers buy at a time when affordability is the greatest conern. There is also the risk of stagflation, which occurs when the rate of inflation increases, while the rate of economic growth slows. We are not on the warning track yet, but last week’s economic data did raise some concerns.

The Economy Is Fragile

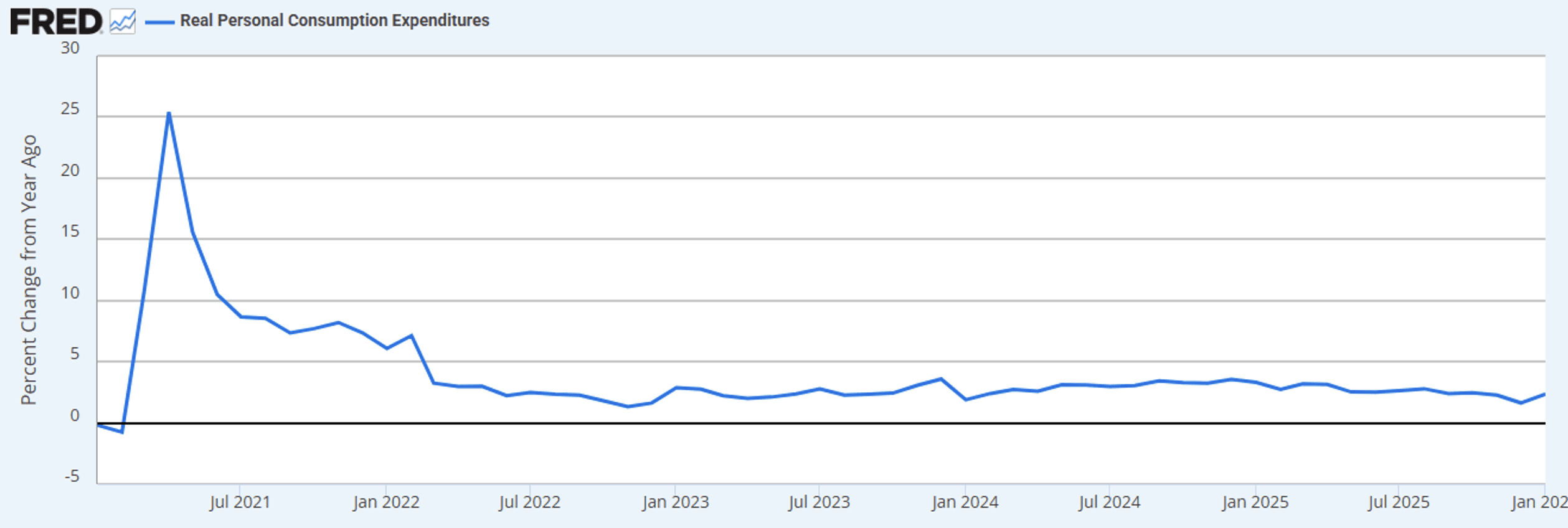

Last week, the Bureau of Economic Analysis lowered its estimate for economic growth (GDP) in the fourth quarter of last year to just 0.7%. AI-related investment spending was a primary driver of that tepid rate of growth, as was consumer spending, which decelerated from 3.5% in the third quarter to just 2% in the fourth. The new year started on a better note with personal spending increasing 0.4% in January, leading to a real (inflation-adjusted) year-over-year growth rate of 2.4%. That is consistent with what we have seen since the expansion started and necessary to maintain trend growth of 2% in the economy.

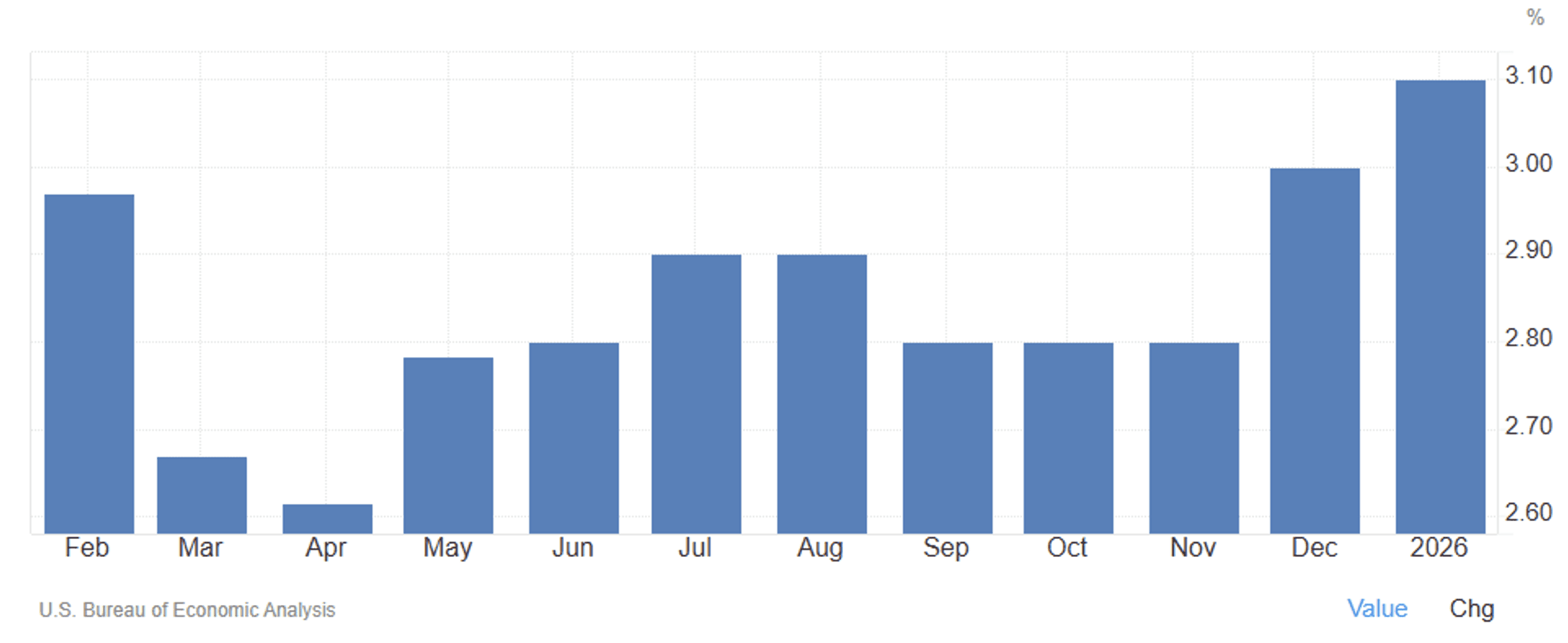

We also had the strongest reading in four years from the ISM Services Index for February, which bodes well for first quarter GDP. The Atlanta Fed increased its estimate for growth in the current quarter to 2.7%. Therefore, we began the war in Iran from a decent level of growth, but the rate of inflation also rose, bringing an end to the disinflationary trend. The core personal consumption expenditure (PCE) price index, which is the Fed’s preferred measure of inflation, rose 0.4% in February and 3.1% on an annualized basis. That is the highest level of core inflation (excludes food and energy) in two years.

This will make it very difficult for the Fed to continue lowering short-term interest rates, as inflation moves further from its 2% target. Furthermore, if oil prices remain high and filter into the cost of goods and services, the rate of inflation could move significantly higher. It would also weigh heavily on the rate of consumer spending, which is the primary driver of growth in our economy.

Reopening The Strait Of Hormuz Is Vital

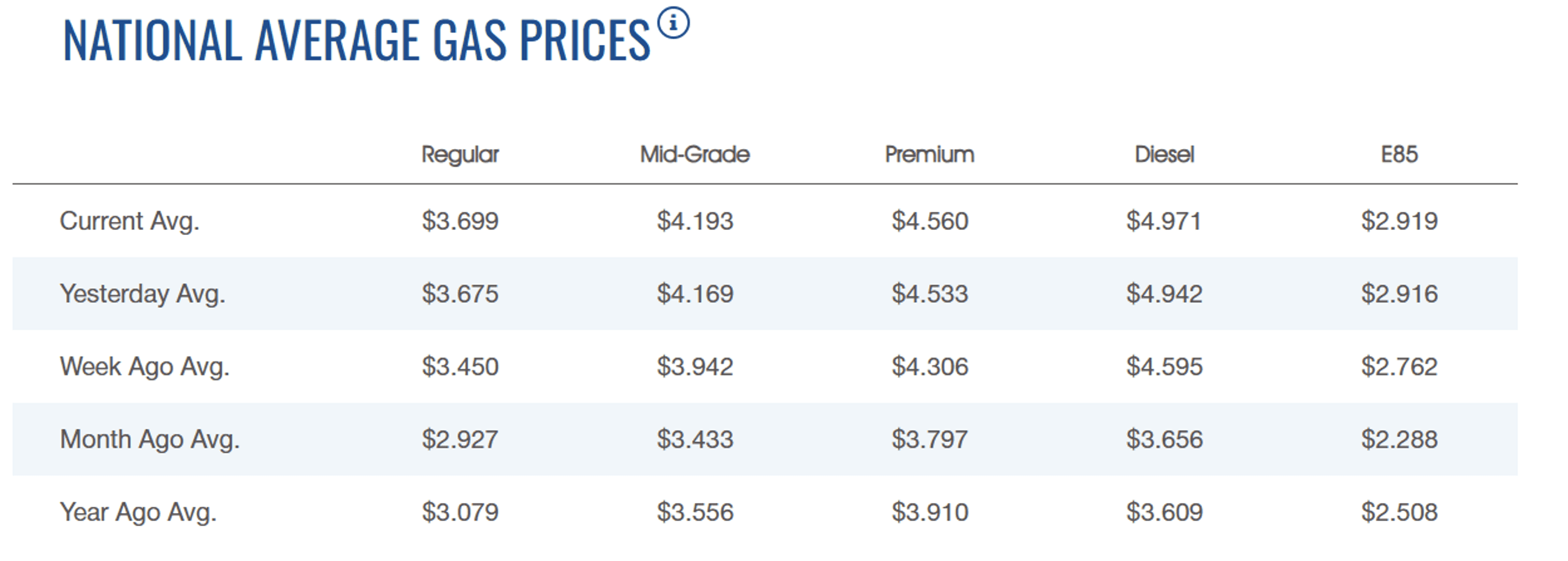

Today, the most meaningful impact from $100 plus oil is on consumers, who are already paying higher gasoline prices at the pump. The national average has risen more than 25% since the war started, and it is likely to increase further in coming days. We are also seeing a significant increase in the cost of airline tickets and other forms of travel. On Friday, the University of Michigan consumer sentiment survey fell to a three-month low, as concerns rose about the impact on fuel prices from the war in the Middle East. According to Joanne Hsu, the director of the survey, interviews that were taken before the attack on Iran showed improvement, but there was a sharp deterioration in the ones taken during the nine days after the war started, which negated the pre-war improvement in surveys.

It is vital that the Strait of Hormuz reopens. This is critical to bringing the price of oil back down to pre-war levels. There have been multiple attempts by the Trump administration to temper the price increase, including the release of 172 million barrels of oil (40%) from our Strategic Petroleum Reserve, plans to use the U.S. Navy to escort oil tankers through the Strait of Hormuz, as well as lifting sanction on Russian oil at sea to increase supply. Nothing has worked, and futures markets indicate higher oil prices on Monday morning.

At the beginning of this war, I asserted the price of oil would dictate when it ended, and that the peak in price would likely coincide with the end of the pullback or correction in the stock market. My greatest concern today is how long it takes to get there, because the longer oil prices remain elevated, the greater the risk that we have irreversible damage to our economy that could undermine the expansion and bull market. If the turning point comes before the end of this month, which is my base case, I think we can sustain both. If it doesn’t, more defensive portfolio positioning will be prudent.

Lawrence Fuller

Founder of Fuller Asset Management & dub Portfolio Creator SeekingAlpha Top Contributor (22k followers)

Background

With three decades of experience in portfolio management, Lawrence commenced his career at Merrill Lynch in 1993 and subsequently held similar roles at various Wall Street firms before establishing Fuller Asset Management in 2005. Since 2013, he has been an esteemed contributing writer for Seeking Akpha, authoring the widely followed Morning Brief newsletter, which boasts a dedicated readership exceeding 22,000 investors.

© 2026 DASTA Incorporated. All Rights Reserved. Performance shown is gross of fees and does not include SEC and TAF fees paid by customers transacting in securities. The dub app is owned and operated by DASTA Inc.. Advisory services provided by Dub Advisors, an SEC registered investment advisor. Past Performance does not guarantee future results. This content is provided for informational purposes only and is not intended as and may not be relied on in any manner as a recommendation or endorsement of any user, portfolio, thematic idea, or ESG factor offered by DASTA Incorporated (DBA “dub”) or its subsidiaries or affiliates (together “dub”). All investments involve risk, including the possible loss of principal. Past performance does not guarantee future results, and investors should consider their own investment goals, risk tolerance, and financial situation before investing. The content herein is not warranted as to completeness or accuracy and is subject to change. The information presented, and its importance is an opinion only and should not be relied upon as the only important information available. The information may contain forward looking statements, including assumptions, estimates, projections, opinions, models and hypothetical performance analysis, which are inherently subjective. Changes thereto and/or consideration of different or additional factors could have a material impact on the statements made herein and Dub assumes no liability for the information provided. Advisory services provided by DASTA Investment, LLC (“Dub Advisors”), an SEC-registered investment adviser. Brokerage services provide by Dub Financial, LLC, and clearing and execution services by APEX Clearing Corporation (“Apex”), both SEC-registered broker-dealers and members of FINRA/SIPC. The registrations and memberships above in no way imply that the SEC, FINRA, or SIPC has endorsed the entities, products or services discussed herein. Additional Information is available upon request.