The AI Divide — Infrastructure Wins While Software Struggles

Apr 27, 2026

•

Libardo Lambrano

Markets Hold Near Record Highs as Earnings Season Broadens

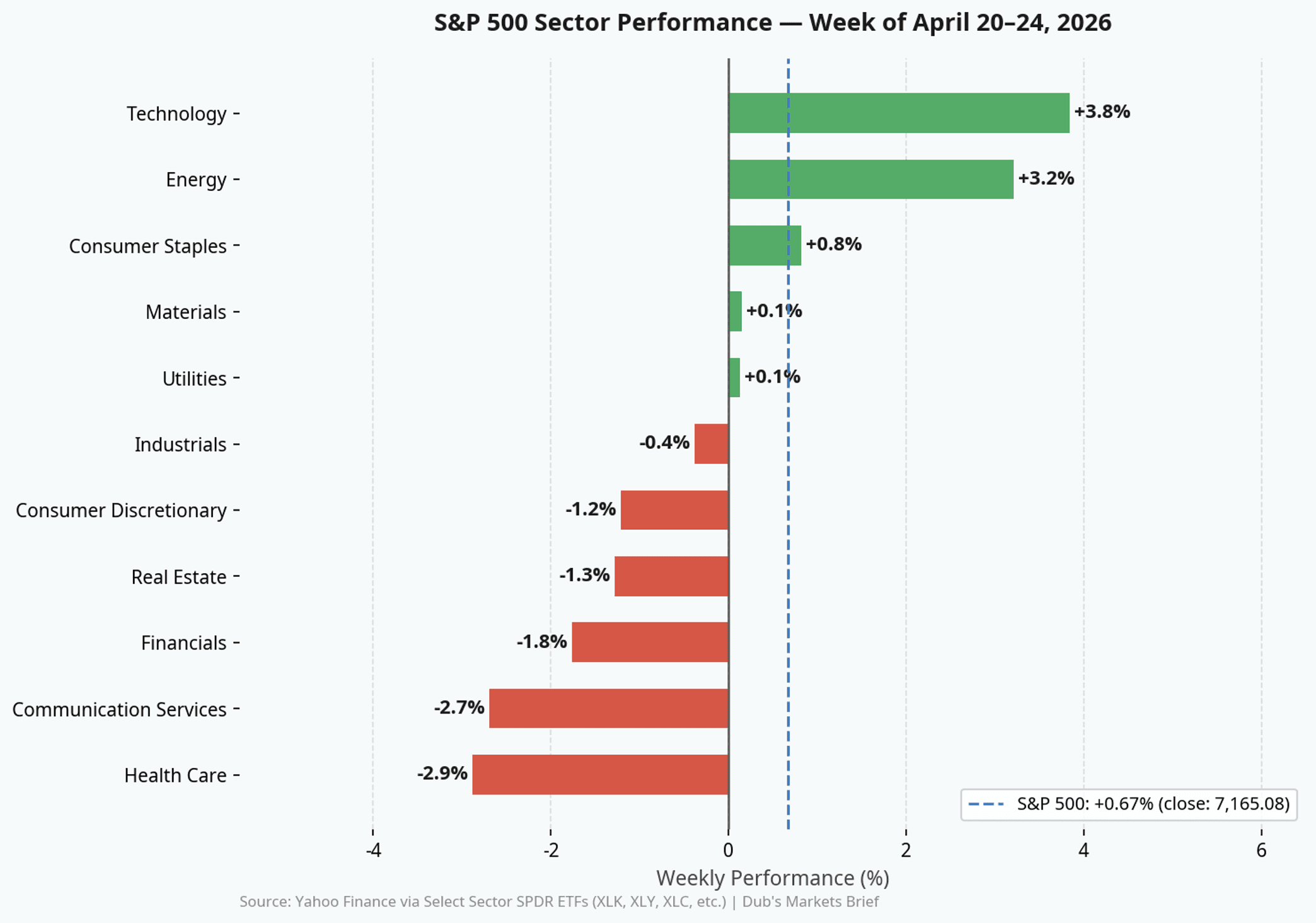

The S&P 500 extended its winning streak this week, adding a modest 0.67% to close at 7,165.08 — building on last week's record close and keeping the index up 4.1% year-to-date [1]. The muted weekly gain belies the significance of what is unfolding beneath the surface: with over 100 companies having reported first-quarter earnings, the picture that emerges is not one of broad strength or broad weakness, but of a deeply fragmented economy where sector outcomes are increasingly determined by a single variable — artificial intelligence [2].

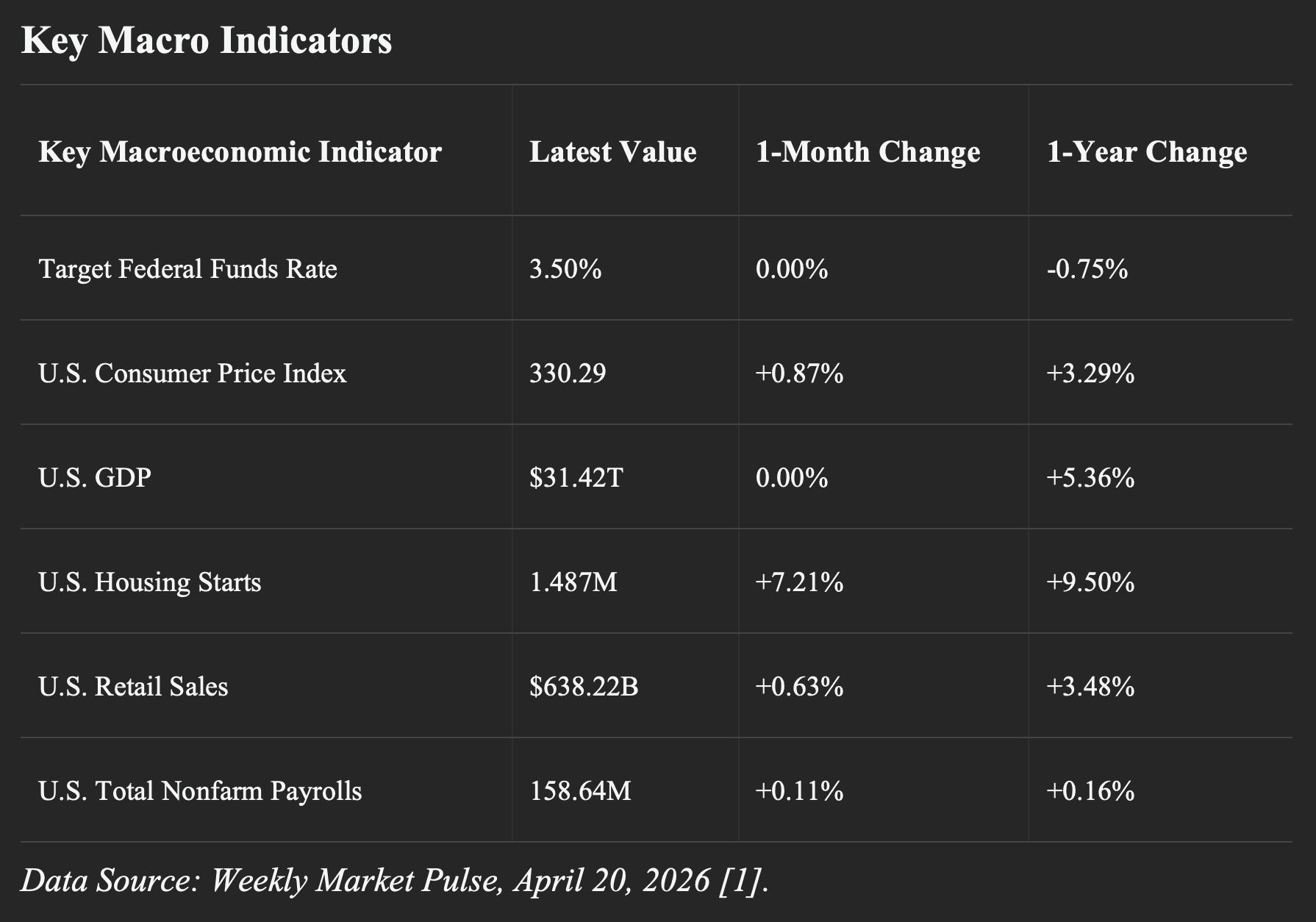

The geopolitical backdrop continues to evolve. Iran's reopening of the Strait of Hormuz during the prior week's ceasefire period provided the catalyst for the market's record close, and peace negotiations appear to be progressing. Yet the conflict's economic fingerprints remain visible. The 10-year Treasury yield has risen to 4.4%, a direct consequence of the inflationary pressures generated by elevated oil prices [2]. That yield level is not catastrophic, but it is consequential — particularly for rate-sensitive sectors that had been counting on a more accommodative environment heading into the spring.

Earnings Season: No Recession Signal, but a Fragmented Economy

The most important macro takeaway from this earnings season is also the most reassuring: there is no recession on the horizon. Large banks continue to report benign credit data, and the breadth of corporate results — spanning industrials, healthcare, financials, and technology — shows an economy that is fundamentally healthy [2]. The results across the board contained nothing to suggest an imminent contraction.

The divergence between sectors, however, is stark. The homebuilding sector is the most visible casualty of the current rate environment. With the 10-year Treasury yield rising to 4.4% — a direct consequence of war-driven inflation — the spring selling season has been materially disrupted. DHI reported home closings below guidance, while Meritage Homes saw earnings per share collapse 51% alongside a 5% decline in year-over-year orders [2]. Airlines are facing a similar squeeze: United and American Airlines both cut 2026 earnings guidance due to higher fuel costs, even as GE Aerospace reported an 87% surge in total orders — confirming that structural aviation demand remains intact despite near-term margin pressure [2].

The AI Divide: Infrastructure Winners vs. Software Under Siege

The most consequential theme of this earnings season is the bifurcation that artificial intelligence is creating across the economy. AI is simultaneously the most powerful tailwind and the most disruptive headwind in today's market, depending entirely on which side of the divide a company sits.

On the infrastructure side, the numbers are extraordinary. GE Vernova reported a 71% year-over-year jump in orders for gas turbines and electrical equipment — the physical machinery required to power the AI data centers being built across the country [2]. This is not speculative demand; it is contracted backlog. The United States is now experiencing electrical demand growth of approximately 3% per year — a remarkable figure given the scale of the existing national grid [2]. Re-industrialization and AI expansion are driving this surge in tandem, and the companies supplying the picks and shovels of this buildout are among the clearest beneficiaries in the market today.

The software sector tells a very different story. Even companies reporting strong fundamental growth are being punished by investors who have lost confidence in the traditional software business model. ServiceNow posted 22% total revenue growth, yet its stock dropped 13% after hours due to slightly delayed deal closings tied to the Middle East conflict [2]. IBM met its software revenue estimates with an 11% increase and still saw its stock fall 7% [2]. The market is not simply reacting to results — it is repricing the long-term earnings power of the entire sector.

The core concern is structural. For decades, the bull case for software rested on two compounding dynamics: growing the number of users on a platform (seat growth) and steadily raising prices per user. AI automation is beginning to undermine both. As AI tools allow companies to accomplish the same workflows with fewer employees, the demand for per-user software licenses naturally contracts. The historical engine of software revenue growth — selling more seats to more people at higher prices every year — is facing its most serious challenge since the industry's inception [2].

The threat is more nuanced than the headlines suggest. In enterprise software, the barriers to replacing incumbent platforms remain high — maintaining custom code, managing regulatory compliance, and absorbing total cost of ownership keeps most organizations anchored to established vendors. The real disruption is not replacement; it is the erosion of pricing power and the slowing of seat expansion that will compress long-term growth rates [2].

The Deficit Debate: Why the Bond Market Is the Real Arbiter

With U.S. debt-to-GDP hitting an all-time high of 125%, deficit anxiety has grown louder in financial media. The concern deserves context, however. Commentators have predicted a debt-driven market calamity for decades without result, and the comparison to Japan — which operates a functioning debt market at a 240% debt-to-GDP ratio, nearly double the U.S. level — is instructive [2]. More practically, if the bond market were genuinely alarmed by the U.S. fiscal position, the 10-year Treasury yield would be trading well above its current 3.9%–4.5% range. U.S. Treasuries remain the backbone of the global repo market, and until a credible alternative emerges, the deficit warrants monitoring but not panic.

The Bottom Line for Investors

This earnings season delivers a clear message: the economy is healthy, but the distribution of that health is uneven and increasingly shaped by AI. Companies supplying the physical infrastructure of the AI buildout — power generation, industrial equipment, aerospace — are benefiting from one of the most durable demand cycles in a generation. Those concentrated in traditional software face a more difficult path, not because businesses are failing today, but because the market is beginning to price in a future where the historical growth algorithm no longer applies.

A durable peace agreement with Iran would relieve energy-driven inflation, ease the squeeze on airlines and homebuilders, and pull the 10-year yield back toward a more supportive level for rate-sensitive sectors. Until that clarity arrives, the market is likely to remain headline-driven — rewarding patience and penalizing overreaction in equal measure.

Libardo Lambrano

dub Premium Creator

Background

Macro investor focused on all-weather, precious metals, and geopolitical risk strategies.

© 2026 DASTA Incorporated. All Rights Reserved. Performance shown is gross of fees and does not include SEC and TAF fees paid by customers transacting in securities. The dub app is owned and operated by DASTA Inc. Advisory services provided by Dub Advisors, an SEC registered investment advisor. Past Performance does not guarantee future results. This content is provided for informational purposes only and is not intended as and may not be relied on in any manner as a recommendation or endorsement of any user, portfolio, thematic idea, or ESG factor offered by DASTA Incorporated (DBA “dub”) or its subsidiaries or affiliates (together “dub”). All investments involve risk, including the possible loss of principal. Past performance does not guarantee future results, and investors should consider their own investment goals, risk tolerance, and financial situation before investing. The content herein is not warranted as to completeness or accuracy and is subject to change. The information presented, and its importance is an opinion only and should not be relied upon as the only important information available. The information may contain forward looking statements, including assumptions, estimates, projections, opinions, models and hypothetical performance analysis, which are inherently subjective. Changes thereto and/or consideration of different or additional factors could have a material impact on the statements made herein and Dub assumes no liability for the information provided. Advisory services provided by DASTA Investment, LLC (“Dub Advisors”), an SEC-registered investment adviser. Brokerage services provide by Dub Financial, LLC, and clearing and execution services by APEX Clearing Corporation (“Apex”), both SEC-registered broker-dealers and members of FINRA/SIPC. The registrations and memberships above in no way imply that the SEC, FINRA, or SIPC has endorsed the entities, products or services discussed herein. Additional Information is available upon request.