The Week in Dispersion

Apr 27, 2026

•

Itai Lourie

Four signals from a regime where the aggregate isn't doing the work.

The market is trading like the war is over. It is not. Hormuz is still closed. Underneath the calm, the cross-asset dispersion signal has risen for eight straight weeks. Pair-trade structures built around the energy shock are showing material divergence in their components. Memory and storage names have run hard, carrying some of the longest unbroken positive directional signals while just registering the largest single-week valuation stretches anywhere in the universe.

We are seeing a regime with an aggregate that is calm at the surface and not calm underneath.

Hormuz: A Historical Lens

History does not repeat itself, but it has a fondness for certain geometries. The most durable is the chokepoint: a narrow passage through which an economy's lifeblood must flow, watched over by a hostile or capricious power. Athens at the Hellespont, dependent on Black Sea grain through a strait Persia eventually closed. Byzantium on the Bosporus, levying a dekate on every passing cargo for centuries. Iran today at Hormuz, where roughly a fifth of the world's oil passes.

The pattern is a worse comfort than most modern energy analysts seem to realize. Chokepoints rarely close — but when they do, dependent powers buckle. Athens did not fall to a battle. It fell to a closed grain route. Strategic petroleum reserves buy weeks, not months. Alternative supply lines exist on paper and, mostly, on paper alone. The structural lesson the ancients offer is clarifying: command of the passage is not the same as command of the vulnerability.

Cross-Asset Dispersion: The Signal Underneath

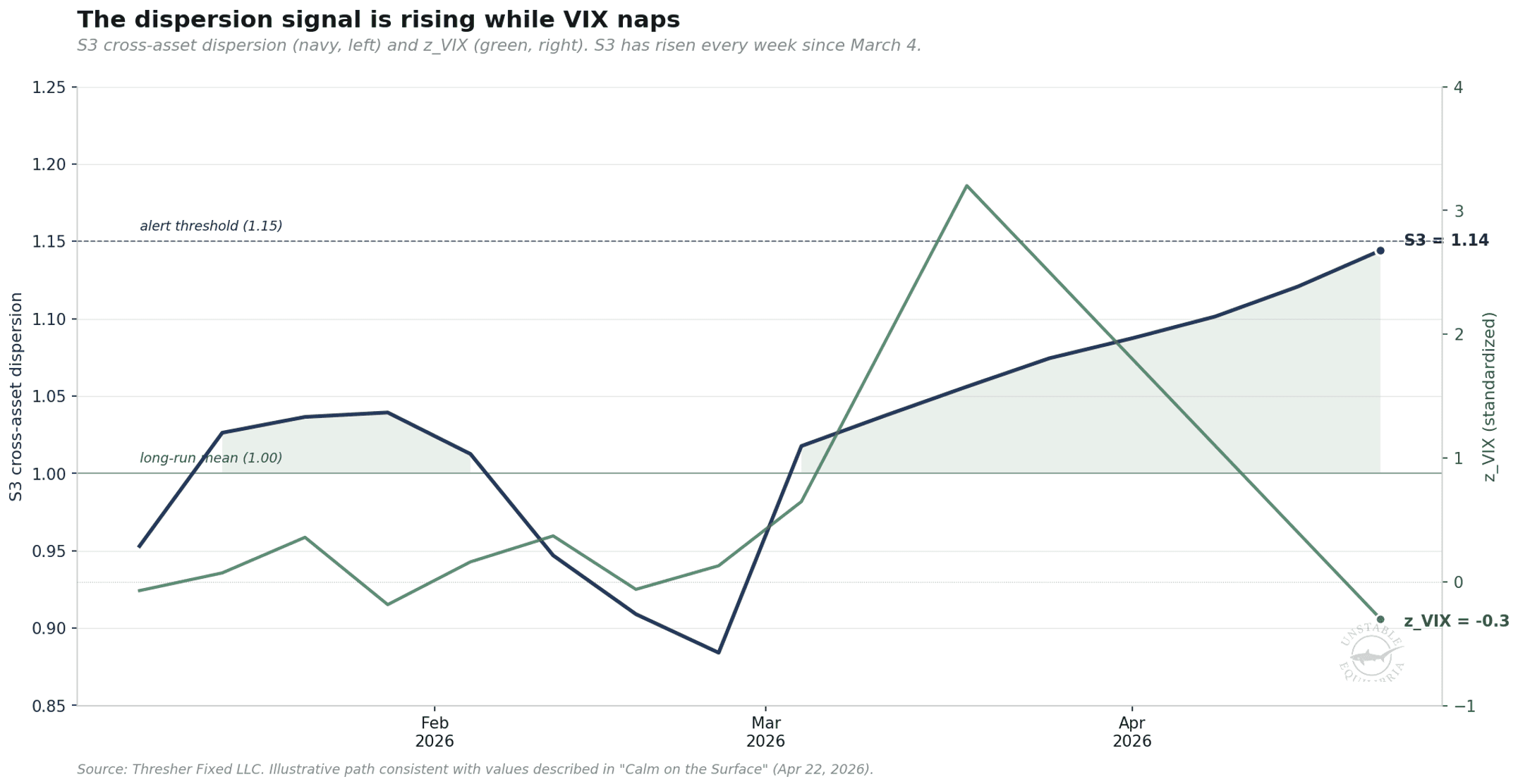

Surface volatility collapsed after the ceasefire rally. VIX dropped. Equities ripped. The cross-asset dispersion signal, a weekly read on whether the pieces of the market are moving together or apart, has not followed it down. Eight consecutive weeks of rise, no pause. Current reading 1.14, against a long-run mean of 1.00 and an alert threshold of 1.15 (proprietary signal).

The dispersion is broad-based. The memory and storage cluster, carrying some of the longest unbroken positive directional signals in equities, registered the three biggest single-week shifts toward expensive in the universe. On the model's z-score convention (positive = cheap, negative = rich), WDC's valuation reading moved from +0.69 to −3.94 in one week. MU moved from −0.70 to −4.63. STX from +1.15 to −2.50. The directional signals on these names have not changed. The valuation signals say the prices have run materially ahead of what the macro environment justifies.

It might not matter.

Outside of excess return credit, bonds are dead money. Copper exited the model; natural gas returned to negative; precious metals and energy held. Industrial metals fading while financial-stress hedges hold is the textbook signature of stalling physical demand without any panic showing in the headline tape.

The aggregate is calm. Underneath, it is not.

Korea / Europe: Divergence Realized

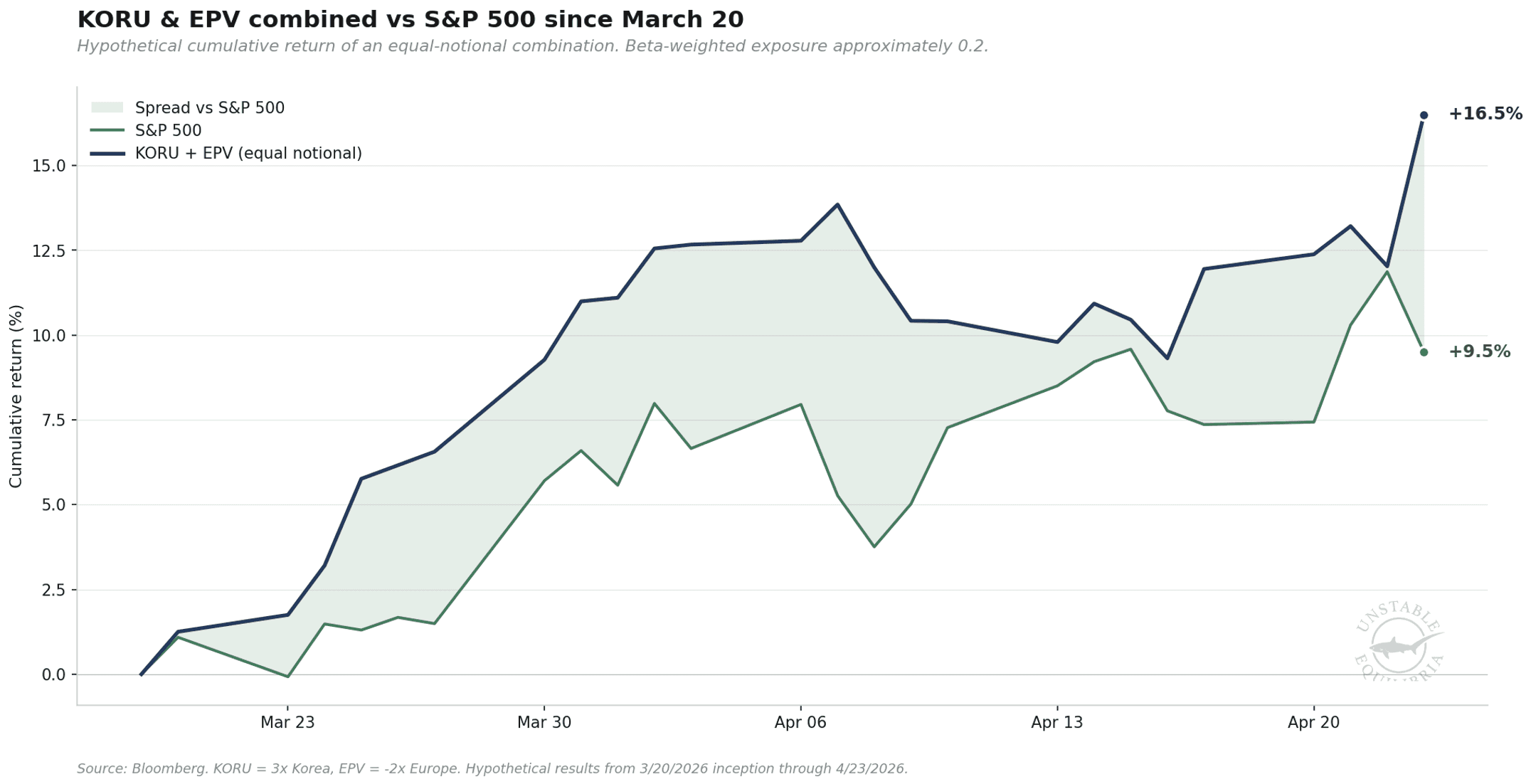

A pair-trade framework of long KORU (3x Korea) against short EPV (-2x Europe), mentioned last week, rests on structural divergence between two categorically different economies. Korea sits at the center of the AI memory cycle with monetary room to ease. Europe is an energy-import-dependent industrial bloc whose central bank is being dragged hawkish by inflation it cannot control.

From the March 20 inception date, with the components held at equal notional weight, the combined hypothetical position would have moved roughly 16.5% over 23 trading days, approximately 7 percentage points above the S&P 500 over the same window, at beta-weighted exposure of about 0.2. Most of the move came from the long leg. KORU appreciated materially since inception; EPV declined only modestly because European equities rallied with the broader risk-on. The thesis has not yet expressed itself fully through the mechanism originally framed, and that distinction matters. The a priori expected return on the framework was 22.2%.

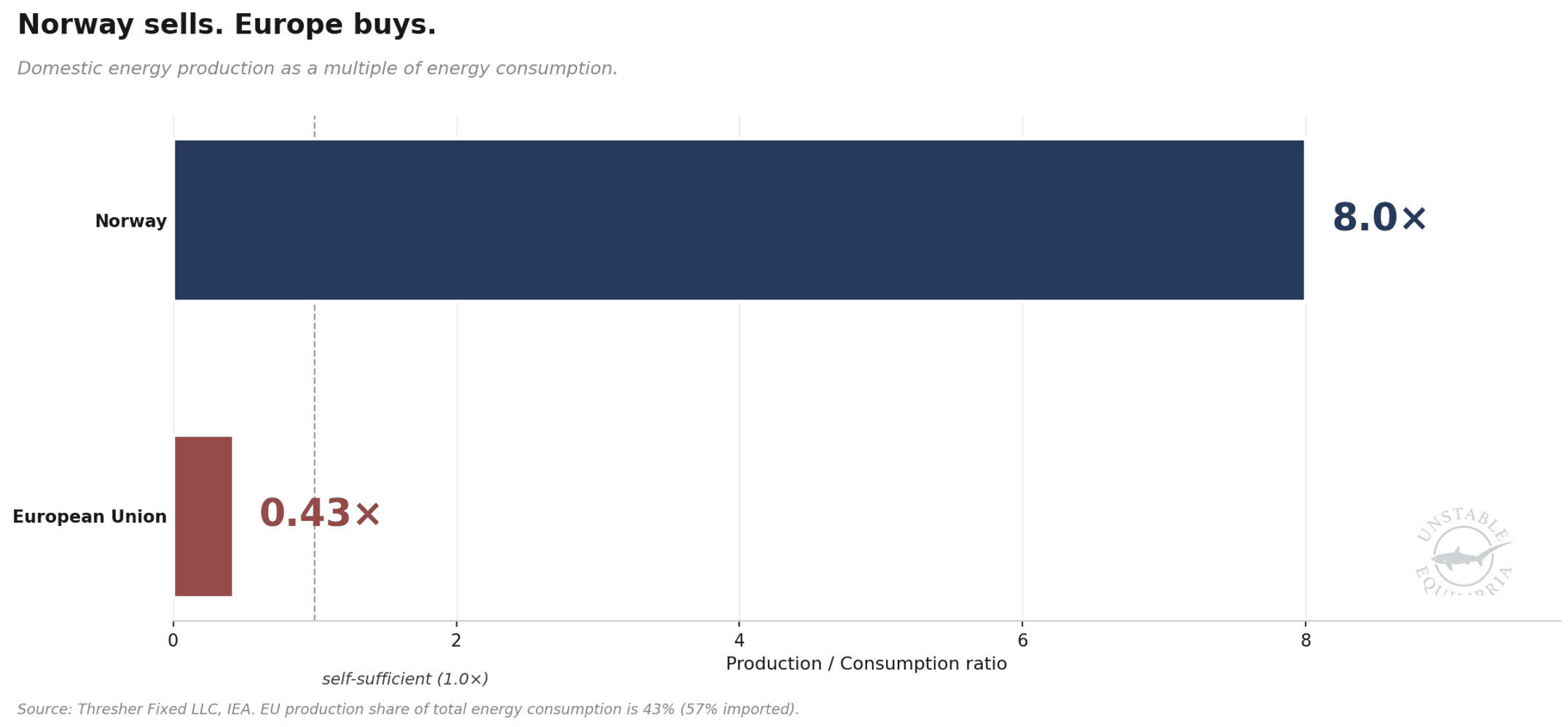

Norway / Europe: The Pipeline Arbitrage

A second pair-trade framework, framed this week, pairs the same EPV short with a NORW long. Where the Korea structure asks who insulates from the energy shock, the Norway one asks who profits from it.

Norway produces nearly eight times the energy it consumes, runs its domestic economy on hydropower, sits on a $1.9 trillion sovereign wealth fund, and runs a 4% policy rate that Norges Bank has signaled will go higher. It exports gas to Germany, missiles to Poland (Kongsberg's Q4 defence book-to-bill ran 2.84, with a January Polish counter-UAS contract that was the largest in the company's history), salmon to Spain, and fertilizer to most of the continent. Every barrel and cubic metre Norway exports is priced in dollars or euros, earned in kroner, and substitutes for almost nothing domestic. Every barrel and cubic metre Europe imports is a transfer out of household budgets, industrial margins, and trade balances.

Four channels do the work in the framework: commodity (Brent at ~$101 with TTF gas dragging European margins), monetary (a hiking Norges Bank against an ECB being dragged hawkish into demand destruction), trade (defence, fertilizer, aluminum, salmon — every Norwegian export keys to a European inelasticity), and currency (a soft krone padding NORW exporters' top lines now, with rate parity arguing for gradual NOK strength later).

Four pieces, one shape. A regime where the aggregate is misleading because the dispersion underneath is doing the real work. Pair-trade structures capture this geometry without taking directional risk on whether Trump chickens out next Tuesday. The same logic applies inside the S&P 500 Information Technology sector – more on that next week.

Itai Lourie

Founder & CIO of Thresher Fixed LLC

Background

Thresher Fixed is a systematic investment manager with deep roots in fundamental, fixed income investing. Our investment framework is a sector agnostic, systematic integration of that value driven heritage with proprietary AI and ML quantitative models. Our strategies include benchmark focused Fixed Income and Total Return.

© 2026 DASTA Incorporated. All Rights Reserved. Performance shown is gross of fees and does not include SEC and TAF fees paid by customers transacting in securities. The dub app is owned and operated by DASTA Inc. Advisory services provided by Dub Advisors, an SEC registered investment advisor. Past Performance does not guarantee future results. This content is provided for informational purposes only and is not intended as and may not be relied on in any manner as a recommendation or endorsement of any user, portfolio, thematic idea, or ESG factor offered by DASTA Incorporated (DBA “dub”) or its subsidiaries or affiliates (together “dub”). All investments involve risk, including the possible loss of principal. Past performance does not guarantee future results, and investors should consider their own investment goals, risk tolerance, and financial situation before investing. The content herein is not warranted as to completeness or accuracy and is subject to change. The information presented, and its importance is an opinion only and should not be relied upon as the only important information available. The information may contain forward looking statements, including assumptions, estimates, projections, opinions, models and hypothetical performance analysis, which are inherently subjective. Changes thereto and/or consideration of different or additional factors could have a material impact on the statements made herein and Dub assumes no liability for the information provided. Advisory services provided by DASTA Investment, LLC (“Dub Advisors”), an SEC-registered investment adviser. Brokerage services provide by Dub Financial, LLC, and clearing and execution services by APEX Clearing Corporation (“Apex”), both SEC-registered broker-dealers and members of FINRA/SIPC. The registrations and memberships above in no way imply that the SEC, FINRA, or SIPC has endorsed the entities, products or services discussed herein. Additional Information is available upon request.