Ugly Economic Data In The Fog Of War

Mar 9, 2026

•

Lawrence Fuller

Stagflation Concerns Give Investors Pause

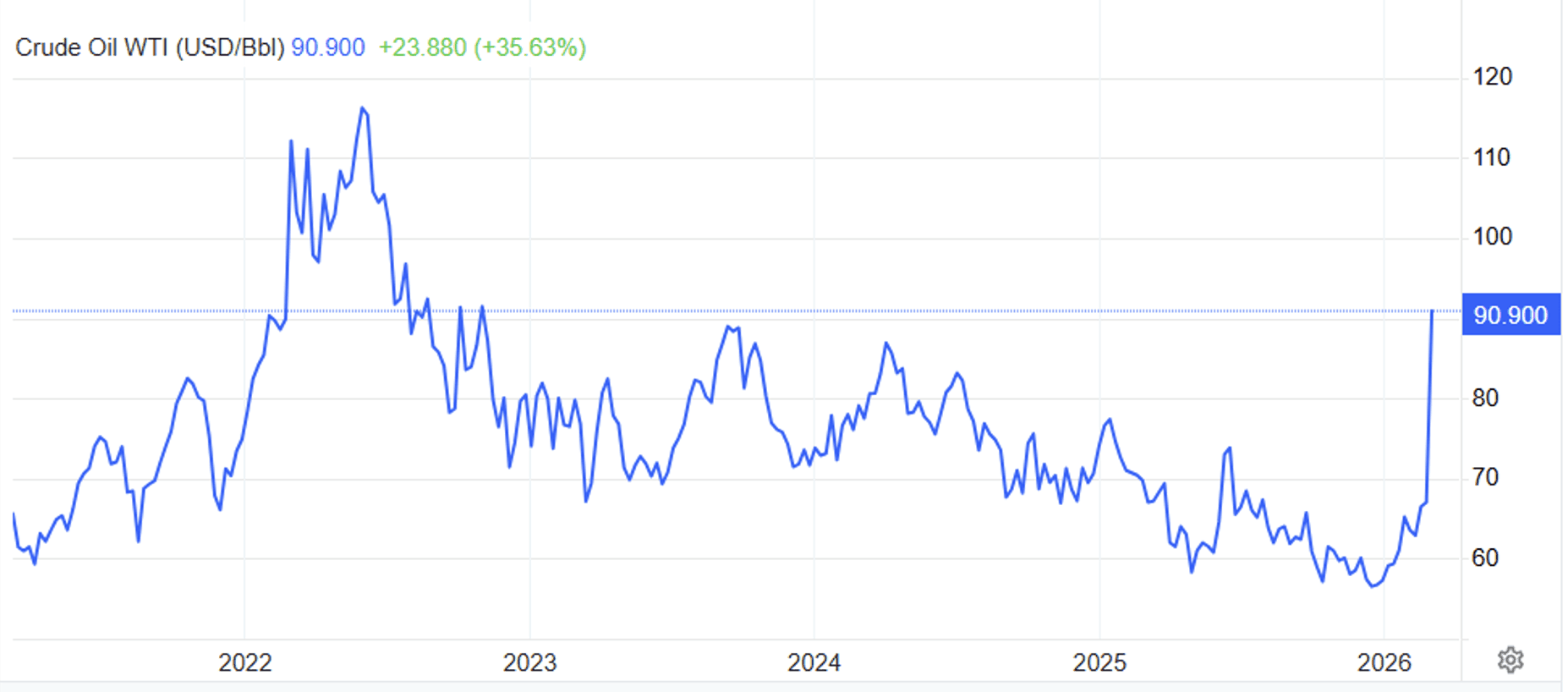

The war in the Middle East moves into its second week, as bombing and unrest spread across the region to neighboring countries. The most relevant impact on the domestic front has been the largest one-week surge in oil prices on record with WTI crude surpassing $92 per barrel on Friday. The rise in energy prices adds insult to injury, as last week’s incoming economic data showed signs of significantly softer growth.

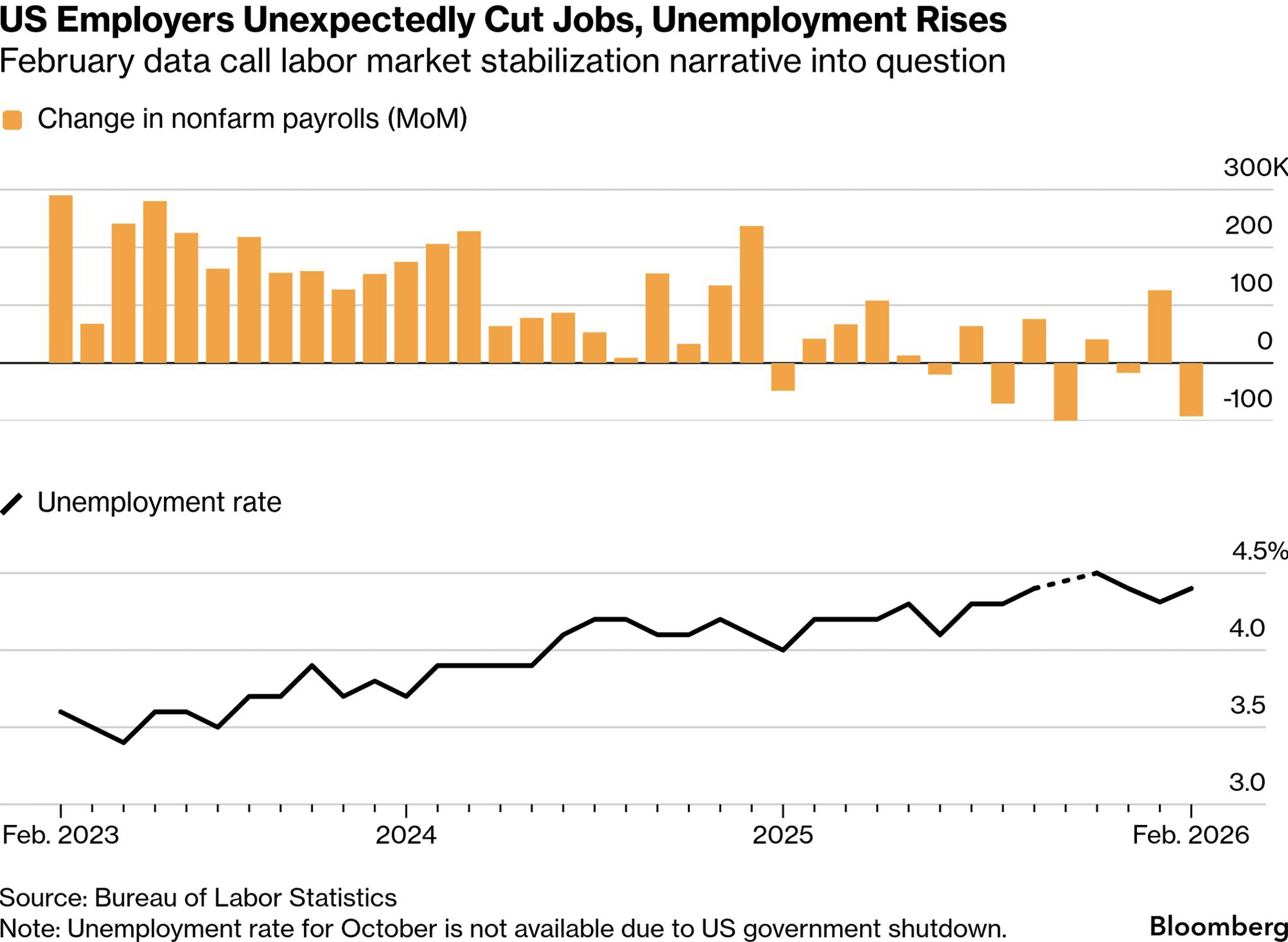

The economy lost 92,000 jobs in what was the worst month for the labor market since the pandemic. Granted, cold weather and some 28,000 healthcare workers on strike negatively impacted the number, but the economy still lost jobs on a net basis. The unemployment rate edged up from 4.3% to 4.4%, while wage growth inched higher to 3.8%. The prior two months were revised lower by 69,000. This kind of stagnation, resulting predominantly from immigration policies and AI-related job losses, can’t continue indefinitely if we are going to maintain trend economic growth of 2%.

Retail sales fell 0.2% in January from the previous month, while control group sales (exclude autos, gas, food, and building materials) used to calculate GDP increased 0.3%. Sales increase 3.2% over the prior year. My main concern here is that sales at bars and restaurants, which is the only service sector of the 13 categories, fell 0.2% in January for the third decline in the past four months. This is the best measure of discretionary spending, and it indicates a cautious consumer. Soaring gasoline prices will not help.

As a result of these reports, the Atlanta Fed lowered its GDP growth estimate for the first quarter from 3.2% to 2.1%. A slowing rate of economic growth in combination with rising energy prices raises concerns about stagflation. Any prolonged period of stagflation would be a major headwind for finanical markets. It would also make the Fed’s job extremely difficult, as it moves the central bank further away from achieving its dual mandate of stable prices and full employment.

Oil Prices May Dictate When The War Ends

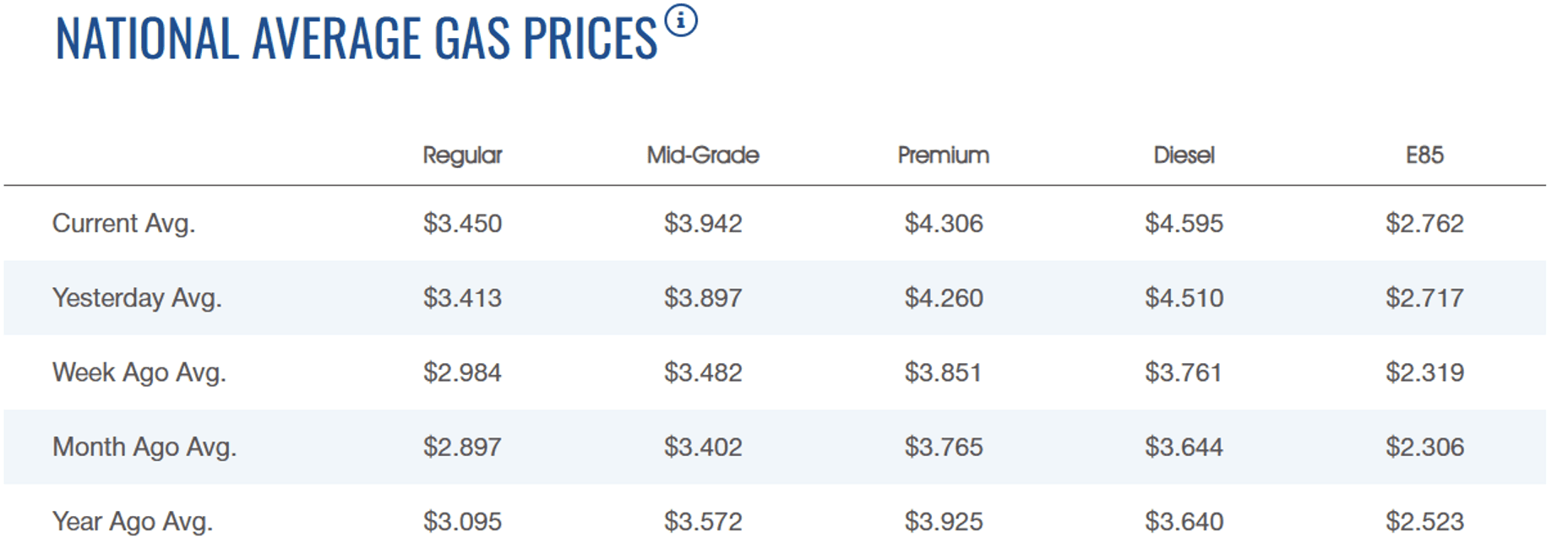

The most immediate impact from rising oil prices is higher gas prices at the pump. The national average has risen from $2.89 a month ago to $3.45 on Sunday, but this does not fully factor in crude over $90/barrel. This rapid price increase could not come at a worse time, given consumers’ concerns about affordability. Every penny increase in gas prices equates to approximately $1 billion in annualized consumer spending power, so the math is simple when it comes to the impact on spending for other goods and services.

Due to the increase in domestic production, our overall economy is less sensitive to rising oil prices than in the past, but should we see oil rise well above $125 on any sustained basis it will raise concerns about a recession. The rapid price increase in 2022 that was caused by Russia’s invasion of Ukraine did not last long, but it did choke growth temporarily. This is why I think oil prices will play a pivotal role in how long this war lasts, as I seriously doubt the Trump administration or the public at large is willing to endure an economic downturn to achieve the outlined objectives in the Middle East. The pullback in the stock market will likely end when oil prices peak. That unknown will keep markets extremely volatile in the days and weeks ahead.

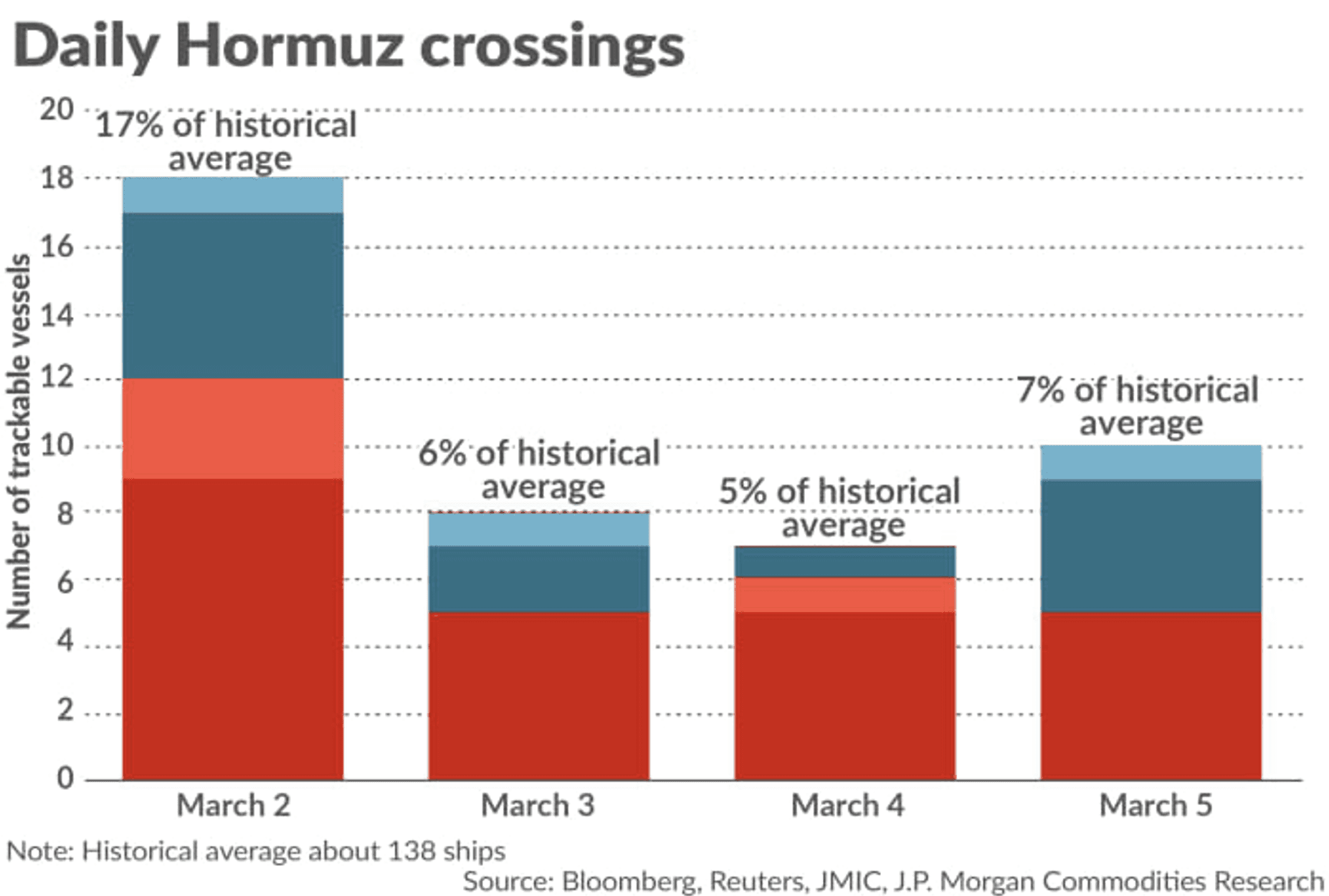

The Strait Of Hormuz Is Choking The Global Economy

Key to lowering the price of oil is reopening the Strait of Hormuz, which is the narrow waterway bordering Iran through which 20% of the global supply of both oil and liquified natural gas flows. Under normal conditions, some 138 container ships pass through this waterway each day, but that number has been reduced by 95% since the war started. There are approximately 400 tankers stuck in the Persian Gulf, and as storage capacity reaches its limits some of the world’s largest exporting countries are starting to halt production, which will put further upward pressure on prices.

On Friday, the Trump administration announced it would provide up to $20 billion in reinsurance coverage for oil tankers and other commercial ships, as well as military escorts, but that has yet to increase activity. Most private insurers have halted coverage. This new insurance is provided through the U.S. International Development Finance Corporation (DFC), but it only has the capacity to provide an additional $130 billion above the $20 billion committed. Meanwhile, the 329 ships currently operating in the Gulf would require more than $350 billion to cover all insurance needs. The President’s announcement was ineffective in stemming Friday’s price increase and escalation over the weekend portend a price north of $100.

I have not lost hope for a continuation of the bull market and economic expansion that underpins it, but we need a deescalation to this conflict over the next couple of weeks, or my optimism wanes significantly. Countering last week’s weak jobs report and soft retail sales data, the ISM Services Index achieved a four-year high in February, albeit before the war started, indicating a reacceleration in economic growth. We also have tax cuts, tax refunds, and now approximately $170 billion in illicit tariff revenue that will be returned to business in coming months. That is a lot spending power. It will be offset to a certain extent by new tariffs and higher energy prices, but the expansion should continue if this conflict ends sooner rather than later.. The depth of the drawdown in the stock market will be a function of how long oil prices remain elevated, the Strait of Hormuz remains effectively closed, and the war continues on. Markets should bottom when oil prices top.

Lawrence Fuller

Founder of Fuller Asset Management & dub Portfolio Creator SeekingAlpha Top Contributor (22k followers)

Background

With three decades of experience in portfolio management, Lawrence commenced his career at Merrill Lynch in 1993 and subsequently held similar roles at various Wall Street firms before establishing Fuller Asset Management in 2005. Since 2013, he has been an esteemed contributing writer for Seeking Akpha, authoring the widely followed Morning Brief newsletter, which boasts a dedicated readership exceeding 22,000 investors.

© 2026 DASTA Incorporated. All Rights Reserved. Performance shown is gross of fees and does not include SEC and TAF fees paid by customers transacting in securities. The dub app is owned and operated by DASTA Inc.. Advisory services provided by Dub Advisors, an SEC registered investment advisor. Past Performance does not guarantee future results. This content is provided for informational purposes only and is not intended as and may not be relied on in any manner as a recommendation or endorsement of any user, portfolio, thematic idea, or ESG factor offered by DASTA Incorporated (DBA “dub”) or its subsidiaries or affiliates (together “dub”). All investments involve risk, including the possible loss of principal. Past performance does not guarantee future results, and investors should consider their own investment goals, risk tolerance, and financial situation before investing. The content herein is not warranted as to completeness or accuracy and is subject to change. The information presented, and its importance is an opinion only and should not be relied upon as the only important information available. The information may contain forward looking statements, including assumptions, estimates, projections, opinions, models and hypothetical performance analysis, which are inherently subjective. Changes thereto and/or consideration of different or additional factors could have a material impact on the statements made herein and Dub assumes no liability for the information provided. Advisory services provided by DASTA Investment, LLC (“Dub Advisors”), an SEC-registered investment adviser. Brokerage services provide by Dub Financial, LLC, and clearing and execution services by APEX Clearing Corporation (“Apex”), both SEC-registered broker-dealers and members of FINRA/SIPC. The registrations and memberships above in no way imply that the SEC, FINRA, or SIPC has endorsed the entities, products or services discussed herein. Additional Information is available upon request.