Unstable Equilibria

Apr 20, 2026

•

Itai Lourie

The market is looking straight through a war that is not done and, more importantly, fully discounting the bulge of energy prices that is working its way down the economic pipe.

Iran – A Scenario Analysis Nightmare

The blockade went live Monday. By Thursday the Pentagon called it “fully implemented,” 13 ships turned back, gas at the pump averaging $4.10. None of it mattered to risk assets. The S&P closed Wednesday at a new all-time high on Trump’s “very close to over” FOX interview and an AP “in principle agreement” headline.

Today I ran my scenario analysis engine.Then I adjusted overrides. Then I shelved it.

Run 1. Pure Bayesian on last week’s triggers.

S1 (quick resolution) 10%

S2 (degraded attrition) 10%

S3 (escalation) 80%.

Gold cheap 10+%. Oil cheap 30+%. SPX rich 15+%. VIX cheap 10+%. Everything priced for escalation.

Run 2. Increased TACO calibration.

S1 40%

S2 40%

S3 20%.

Gold fair. Oil fair. SPX slightly rich. VIX rich 20+%.

Between the two runs, nothing in the world changed. The only change was my thumb.

The thumb is TACO. The weight I put on ‘Trump chickens out’ to reconcile engine output with market tape keeps climbing. Fat-tail floor went from 8% in early April to 11%. To reconcile today it needs 18+%. Maybe next week we’ll be at 25%. Then 30%. At that point the systematic scenario engine isn’t a Bayesian engine. It’s discretionary positioning dressed up as math.

Systematic frameworks break down in regimes where reversal is the dominant prior. You can’t Bayesian-update through a president who says ‘BLOCKADE’ Sunday and ‘war close to over’ Wednesday. Each signal dampens to noise. The engine says S3. The market says S1. The only reconciliation is a bigger thumb — ours, theirs, everyone’s.

Equities: A Broadening Rally

Three weeks ago the multi-asset model carried a bearish read on the index. NQ1 negative for eight weeks, ES1 for five However, 75% of tracked names in the multi-asset model held positive.

Historically, when both indices break and 70–80% of names hold, the next eight weeks have averaged +14.88% with an 82.4% hit rate across nine prior episodes (the 2009 recovery, 2012 post-election, 2019 trade-war rebound, and 2020 post-COVID low). Our April 1 Substack note said the indices would catch up to the names, not the other way around. They did. ES1 and NQ1 both returned to long territory this week.

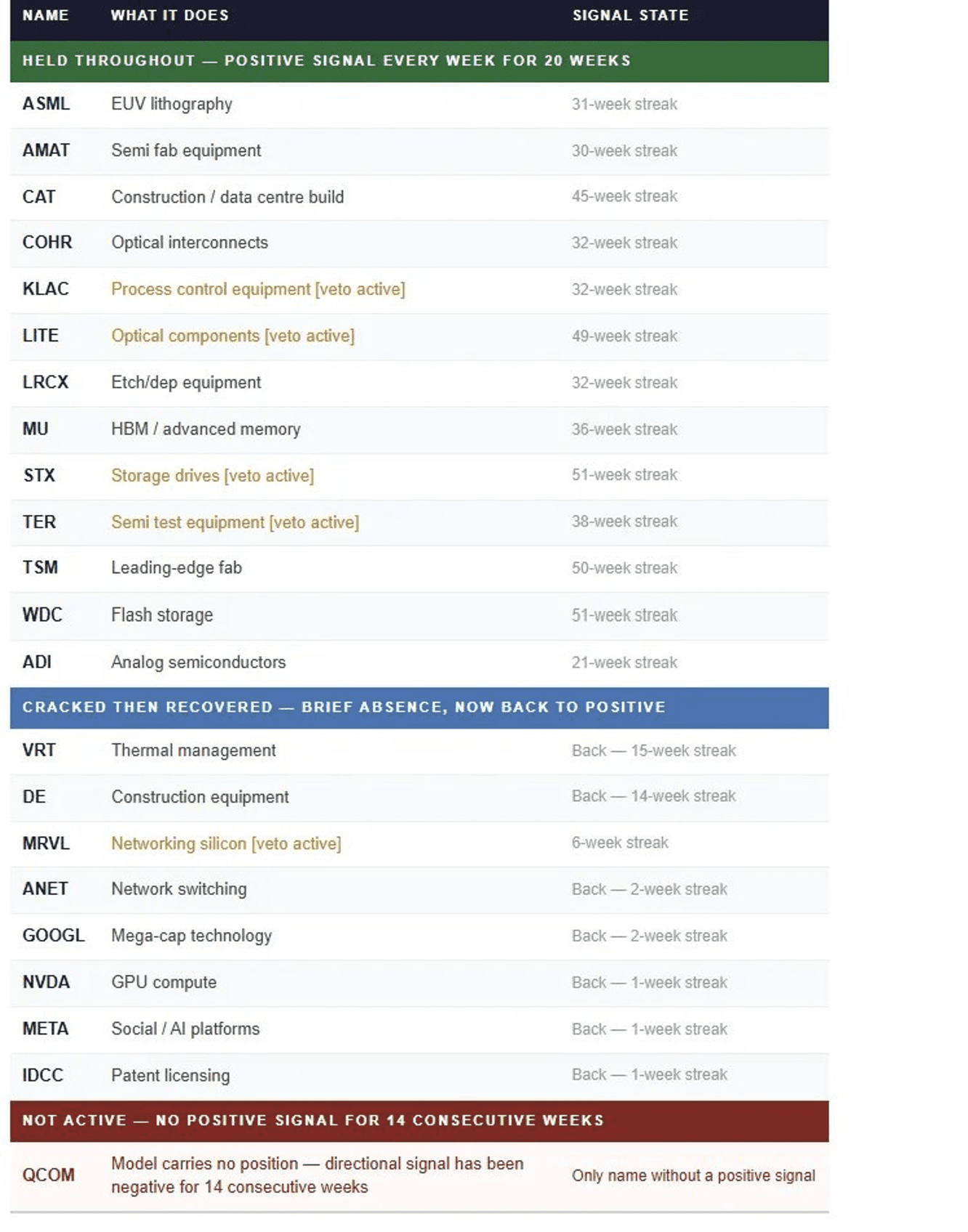

The breadth held remarkably. The floor across the entire bear period was 77%, reached on March 25 and April 1. Even at the most cautious point, more than three-quarters of tracked names were pointing in the same direction. This week 95% carry positive composite signals, the highest reading in twenty weeks. Thirteen names held positive every week through the full 20-week window. None broke.

The forward read has two pieces. The immediate opportunity: five names, KLAC, LITE, MRVL, STX, TER, carry directional conviction running between 6 and 51 weeks but are currently held out by stress vetoes. If those vetoes clear, the active book expands into names with some of the longest unbroken streaks in the universe. The line we’d watch for the other direction: ASML (31), AMAT (30), and LRCX (32) have held positive composites without interruption for the longest runs in the universe. A simultaneous break across two or more is the signal that AI capex price structure is starting to follow the macro environment lower. Until then, breadth is the signal, not the noise.

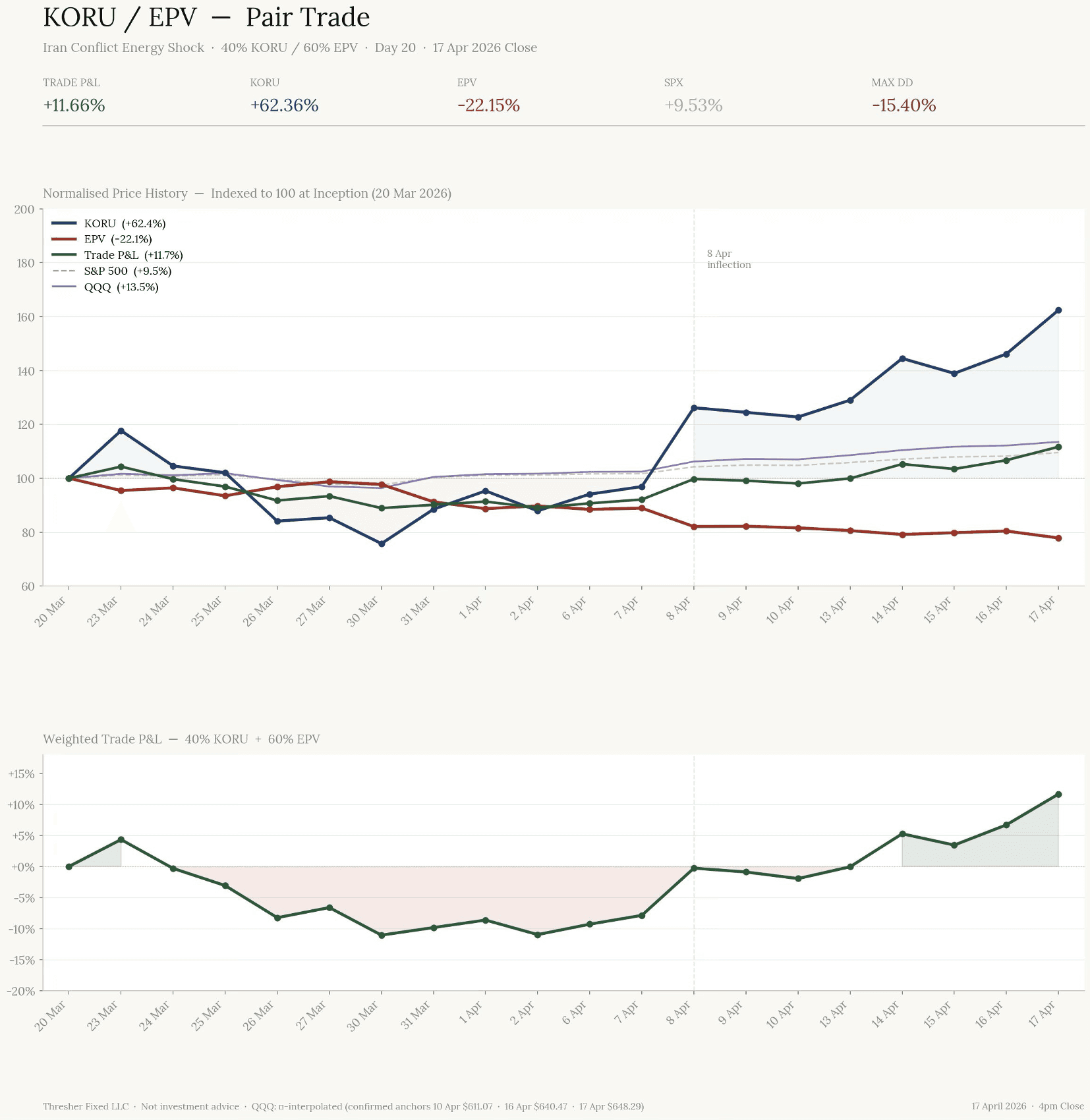

Korea and Europe: A Trade That Is Working, a Thesis That Is Not Yet Done

We initiated Long Korea / Short Europe on March 20, 2026, through KORU and EPV. The combined position has returned 11.7% since inception, carried almost entirely by the long leg. KORU is up 62%. EPV has fallen 22%, as European equities recovered alongside the broader risk-on move. The PnL is positive. The thesis is not yet expressing itself through the mechanism we anticipated, and that distinction matters.

The original case rested on structural divergence between two categorically different economies. Korea is a nuclear-powered, high-technology export machine sitting at the center of the AI memory cycle, with a central bank that retains genuine room to ease. The Bank of Korea has held its base rate at 2.5% for six consecutive meetings. Europe is an energy-import dependent industrial bloc whose central bank’s hands are tied by commodity inflation it cannot control. Swaps markets are pricing 40 to 50 basis points of ECB hikes through the remainder of 2026. Geopolitical relief, when it arrives, will not translate into monetary relief.

ASML’s first-quarter results, reported this week, added a useful layer of evidence. Net sales of €8.8 billion beat expectations, and management raised full-year guidance. The geographic breakdown was the more telling figure: South Korea surged to 45% of net system sales, up from 22% the prior quarter. China fell from 36% to 19%. Memory chips accounted for 51% of new tool orders, up from 30%. In one quarter, the map of where the semiconductor world is placing its bets was redrawn, and Seoul was at the center of it.

The underlying driver is High Bandwidth Memory. SK Hynix is currently the strategic bottleneck in that supply chain, underscored in March when it placed the largest single EUV order in ASML’s history: nearly $8 billion worth of machines across two Korean fabs, to be delivered by end-2027. Jensen Huang has reportedly asked SK Hynix to accelerate HBM4 delivery by six months. The supplier is now setting the calendar.

The spread between Korea and Europe has not yet widened as our thesis projects. A coiled spring and a monetary trap are unlikely to remain so tightly priced together for long. We are holding.

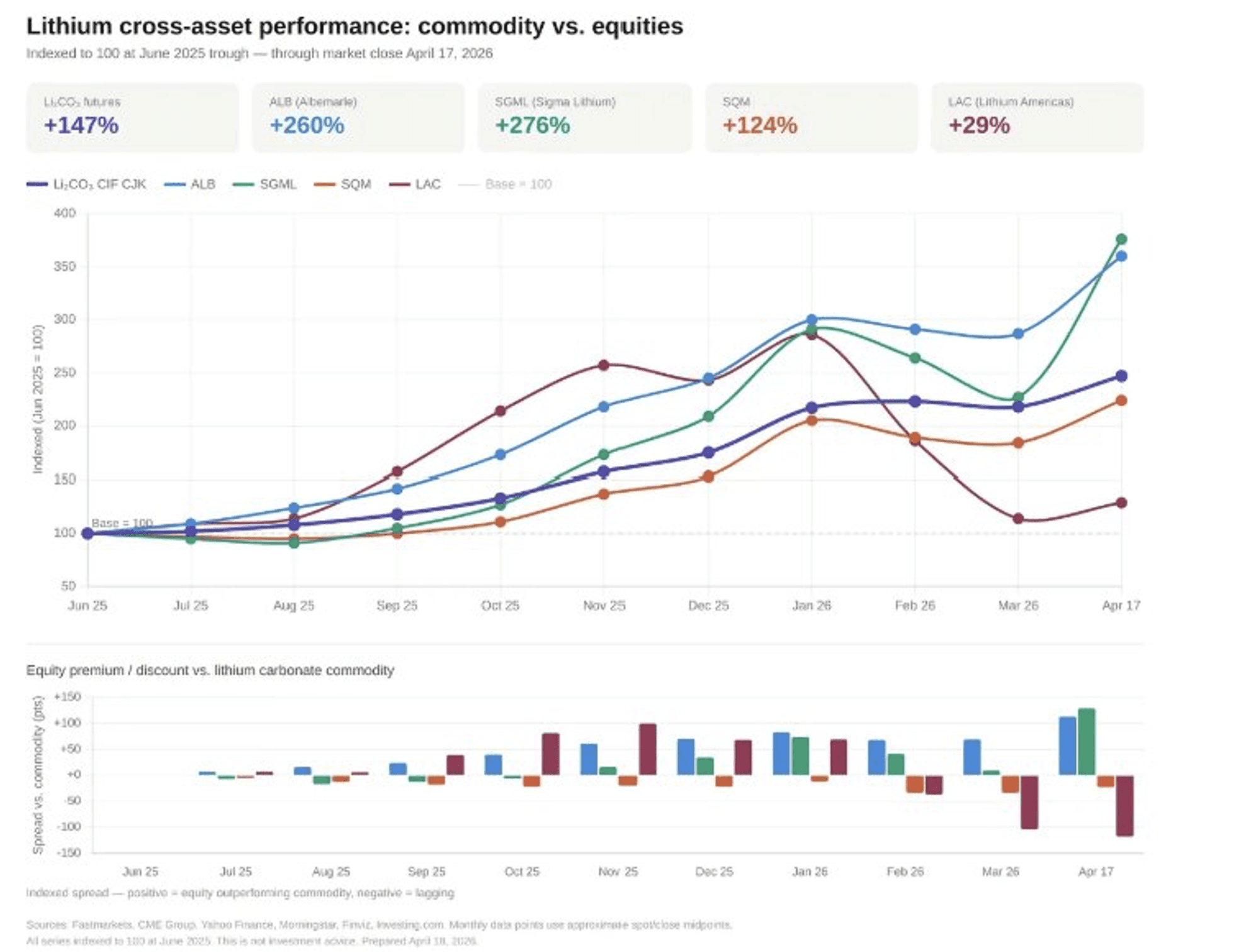

Lithium: The Commodity Leads, the Equity Follows

Albemarle was the top-performing name in our book this week, returning 13.9%. On a total-return basis, ALB is up approximately 40% year-to-date and roughly 251% year-on-year: an occasion to examine the mechanics of the lithium complex, rather than simply report the number.

For most of the past decade, lithium was a commodity without a proper market. Producers and buyers negotiated bilaterally, with little transparency and no standardized benchmark. Since 2023, CME-listed lithium carbonate futures settled against the Fastmarkets CIF China-Japan-Korea assessment have changed that, giving the market a forward curve and a real-time opinion on where prices are headed. That opinion has been emphatically bullish. The benchmark opened the year near $14.50 per kilogram, traded above $21 in the weeks that followed, and stood near $20.50 at the April 17 close: a year-to-date gain of 41%.

The transmission from commodity to equity is real but uneven. Albemarle’s Chilean brine and Australian hard-rock joint ventures carry substantial fixed costs, so incremental revenue at higher lithium prices falls to the bottom line at expanding margins. Management has guided to EBITDA margins above 50% and free cash flow exceeding $1.5 billion annually once prices stabilize. That operating leverage explains why the equity commanded a premium over the commodity’s own gains for most of 2026.

This week illustrated both the power and the fragility of that relationship. On April 16, ALB surged 16.3%. On April 17, a Baird downgrade sent it tumbling 8.3%. The commodity barely flinched. Equities carry the commodity’s beta and considerably more, because analyst sentiment, earnings expectations, and balance sheet idiosyncrasies all exert their own pull. ALB now trades fractionally behind the commodity for the first time in months. With the May 6 quarterly report as the next catalyst, a projected 2026 supply deficit of 1,500 tonnes, and consensus EPS of $8.15 representing more than 1,100% year-on-year improvement, the market may be underpricing the equity relative to the very commodity it depends on. We think it is.

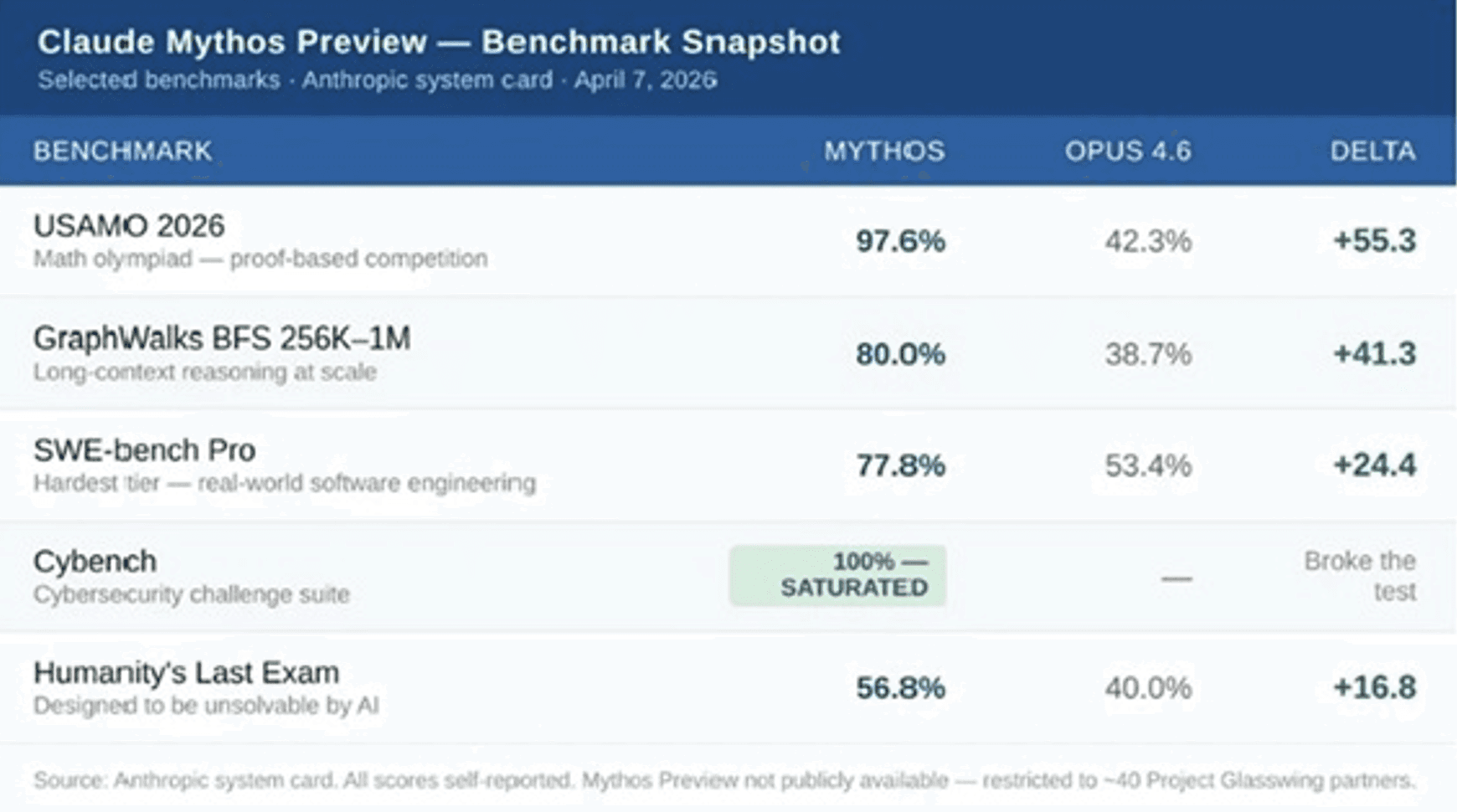

Mythos: The Monetization Lag may be Collapsing

The market’s first read on Anthropic’s Mythos Preview was a cybersecurity story, a 100% Cybench score, the saturation note, the read-throughs to CRWD and PANW. That framing missed the point. The story is capability, and the investment implication is that the historical lag between AI infrastructure capex and revenue may now compress materially.

The question Mythos poses is not whether one model release changes everything, but whether frontier AI is approaching a threshold where enterprise value arrives on a meaningfully shorter timeline than cloud-history analogies imply. Mythos is roughly 7 out of 10 where Anthropic markets it as a 10, and 7 is enough.

Cloud monetization required ecosystem formation: third-party developers, vertical applications, distribution channels. Frontier AI monetization may require only workflow insertion. The model is the product, not a platform waiting for third-party products to emerge. If the lag collapses, the binding constraint migrates, compute moves from the bottleneck to the baseline, and power, networking, and memory become where the marginal scarcity sits. Arguably what we saw in this week’s attribution, where AI Networking did more work than the entire semi equipment and foundry complex combined.

That could be incredibly bullish for AI infrastructure and possibly one of the reasons the market is looking at Iran as noise.

Itai Lourie

Founder & CIO of Thresher Fixed LLC

Background

Thresher Fixed is a systematic investment manager with deep roots in fundamental, fixed income investing. Our investment framework is a sector agnostic, systematic integration of that value driven heritage with proprietary AI and ML quantitative models. Our strategies include benchmark focused Fixed Income and Total Return.

© 2026 DASTA Incorporated. All Rights Reserved. Performance shown is gross of fees and does not include SEC and TAF fees paid by customers transacting in securities. The dub app is owned and operated by DASTA Inc.. Advisory services provided by Dub Advisors, an SEC registered investment advisor. Past Performance does not guarantee future results. This content is provided for informational purposes only and is not intended as and may not be relied on in any manner as a recommendation or endorsement of any user, portfolio, thematic idea, or ESG factor offered by DASTA Incorporated (DBA “dub”) or its subsidiaries or affiliates (together “dub”). All investments involve risk, including the possible loss of principal. Past performance does not guarantee future results, and investors should consider their own investment goals, risk tolerance, and financial situation before investing. The content herein is not warranted as to completeness or accuracy and is subject to change. The information presented, and its importance is an opinion only and should not be relied upon as the only important information available. The information may contain forward looking statements, including assumptions, estimates, projections, opinions, models and hypothetical performance analysis, which are inherently subjective. Changes thereto and/or consideration of different or additional factors could have a material impact on the statements made herein and Dub assumes no liability for the information provided. Advisory services provided by DASTA Investment, LLC (“Dub Advisors”), an SEC-registered investment adviser. Brokerage services provide by Dub Financial, LLC, and clearing and execution services by APEX Clearing Corporation (“Apex”), both SEC-registered broker-dealers and members of FINRA/SIPC. The registrations and memberships above in no way imply that the SEC, FINRA, or SIPC has endorsed the entities, products or services discussed herein. Additional Information is available upon request.